Mobile Banking is Evolving: 7 Key Trends in 2021 & 2022

Market Researcher

Wondering why the cost to develop a mobile banking app grows every year?

The industry changes swiftly and is adopting advanced technologies such as blockchain, big data, machine learning, and Artificial intelligence (AI). Developing and integrating these features requires more time, resources, and professional expertise. Consequently, end-product costs rise as well.

However, the effort and investment are worth it; newer technologies enhance user experience and lead to greater user satisfaction with your product. The Covid-19 pandemic has accelerated the shift to mobile banking, urging financial institutions to adjust customer retention strategies, and to seek more sophisticated and safe remote banking tools.

So which technologies are a worthy investment? Here, we look closely at the key mobile banking trends in 2021 and 2022. But first, let’s examine how Covid-19 has influenced the industry.

How digital banking changes during the Covid-19 pandemic

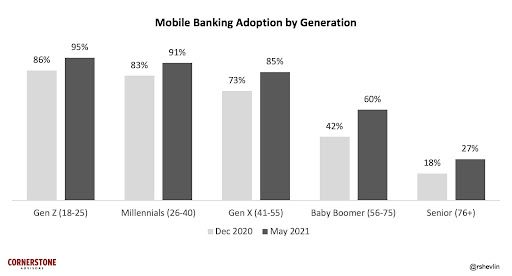

In 2021, 95% of gen Zers, 91% of millennials, 85% of gen Xers, 60% of baby boomers, and over 50% of seniors in the US with a smartphone actively use mobile banking. During the past year, seniors and boomers were nearly as likely to check their account balances via mobile devices as younger customers, and more likely to have used a mobile banking app to pay a bill or deposit a check.

The number of users skyrocketed in comparison to 2018 when only 47% of the US millennials and 23% of baby boomers used mobile banking services. Covid-19 was the main reason behind the sudden uptick in the adoption of mobile banking. Due to continuous lockdowns, customers are unable to visit banks and were forced to use mobile devices for routine tasks such as paying bills and making transfers.

In April 2020, new mobile banking registrations surged 200% and mobile banking traffic rose 85%, according to Fidelity National Information Services (FIS). Banks associate the surge in demand not only with the inability to visit physical branches, but also with stimulus checks; users who checked their balance once in a while suddenly began to check several times daily.

Banks are also seeing a major rise in remote deposits and online account openings. The head of Key Bank's digital banking department states that the bank saw double-digit growth in online usage every month. It seems that customers are starting to appreciate the comfort and convenience of mobile banking.

US bankers expect the number of mobile banking users to rise further, even in the aftermath of the Сovid-19 crisis when restrictive measures ease. “Once people begin favouring mobile-based account access, there’s no going back," says Maria Schuld, a representative of FIS North America. Financial institutions have to adopt digitalisation quickly as very soon, a bank without a mobile app will be the same as a non-existent one.

Moreover, to remain competitive, banks and fintechs have to be on the cutting edge of innovation. This means that not only banks should improve their app speed, but also cover customers’ needs better. The main focus of mobile banking for the next few years is to make the banking app experience seamless and as comfortable and secure as possible.

7 trends of mobile banking in 2021 & 2022

Here are the major mobile banking trends that are building an increasingly user-centric environment, and providing an advanced experience. Let’s take a closer look.

Touchless transactions and ATM connectivity

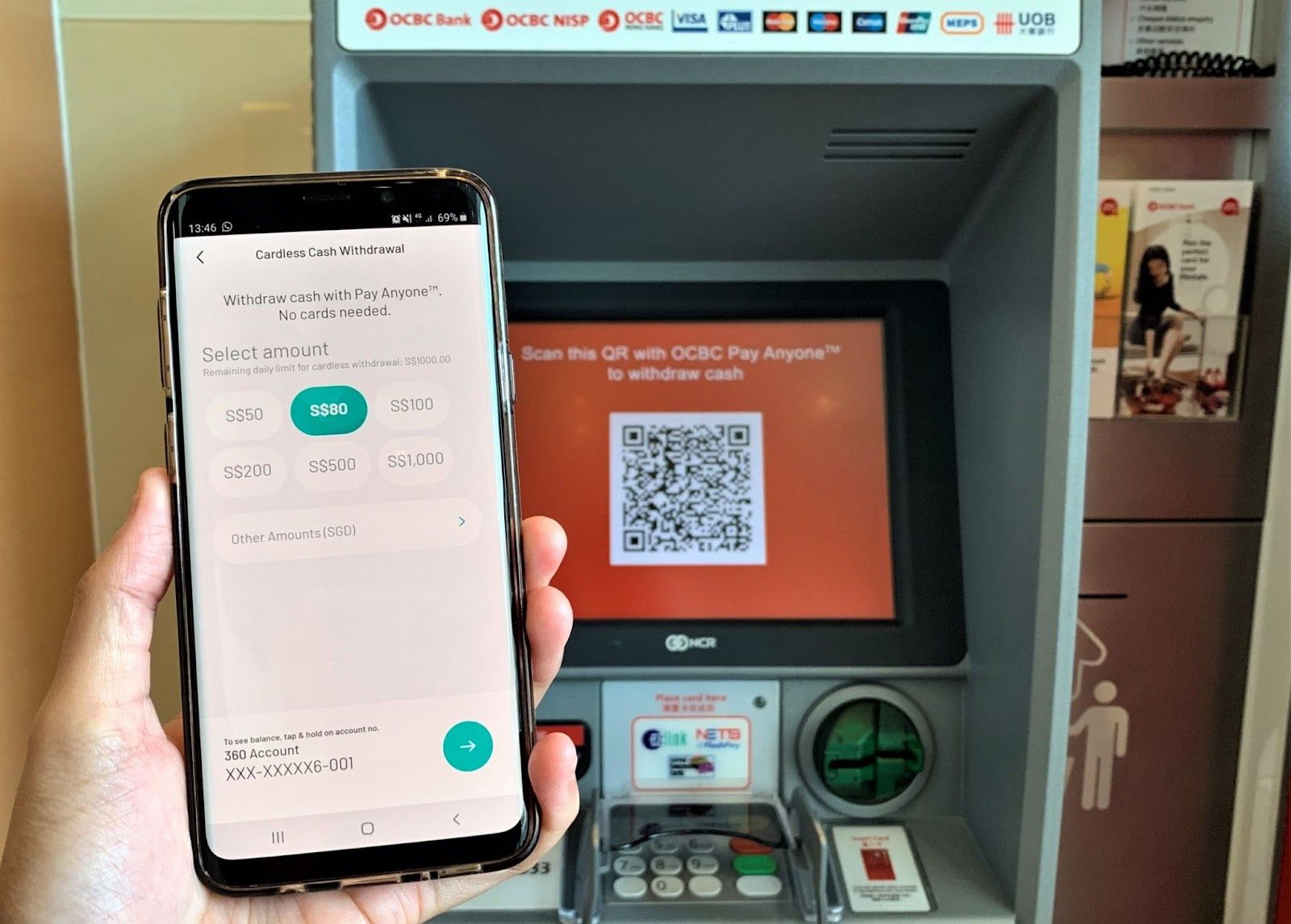

Screen-based QR codes are already a popular way to authenticate touchless transactions in stores or on public transport, and this trend is expected to expand significantly in coming years. Advanced communications technology and QR code scanning will soon allow users to interact with ATMs via the bank’s mobile app.

Source: OCBC Bank

Customers scan the QR code that appears on the ATM screen, then all operations — entering a PIN, specifying a withdrawal amount, and so on — are performed via the app. The technology is highly secure as QR codes not only make withdrawals faster, but also reduce the chances of card skimming or compromised PINs.

Personalisation

Mobile banking users want transaction-based insights to make informed decisions about their finances. Responding to this demand, major banks such as JP Morgan now offer AI-powered services that provide daily transaction updates as well as customised financial advice and reminders to pay recurring bills or make savings.

Source: JP Morgan

Not only are these personalisation efforts good for customers, but for the financial institution as well. Investments in AI pay off as banks or fintech companies can capitalise on an advertising channel for additional products and affiliate financial services. In addition, by creating a personalised environment, banks gain another instrument for customer retention.

Voice Command

Voice tech enables operations within seconds — users just need to ask their smartphones to perform an action and it happens, saving time and making mobile banking more accessible than ever. Tapping on a screen is still a barrier for people with disabilities, for instance. Addressing this issue, many businesses (Walmart, Starbucks, Nike) are already adopting voice payments to improve the digital shopping experience.

At this point, voice technologies appear to offer banks an exciting opportunity to recover lost revenue from tech and fintech players. Despite concerns, voice command functionalities don’t weaken a mobile app’s security. Instead, this technology can be used as an additional level of biometric security. Advanced voice recognition helps verify user identity much like face or fingerprint recognition.

Chatbots

Chatbots and virtual assistants simplify and enhance customer support. A chatbot is AI-powered software that simulates a text-based chat or voice conversation with users through mobile applications, messengers, and websites and is often used to answer frequently asked questions. A chatbot answers up to 80% of routine questions and expedites response times.

Human assistance is still needed as chatbots cannot resolve complex problems, but they can significantly reduce the support department’s workload, freeing agents for more complicated work. According to Chatbots Magazine, businesses can cut up to 30% of their customer service costs by implementing chatbots and/or virtual assistants.

Using Big Data for fraud prevention

Banks have been able to detect and block suspicious transactions or blatant fraud for many years already. For example, a provider can freeze a bank account if the same credit card is used in San Diego at 6 pm, and then in Philadelphia at 6:20 pm the same day. Now, big data brings fraud detection to another level.

Big data fraud detection systems recognise previously learnt patterns and then search for these in datasets to detect and prevent suspicious activity. In other words, AI-based algorithms analyse customer information and predict general trends, helping spot fraudulent transactions before a customer even knows their card or account is compromised.

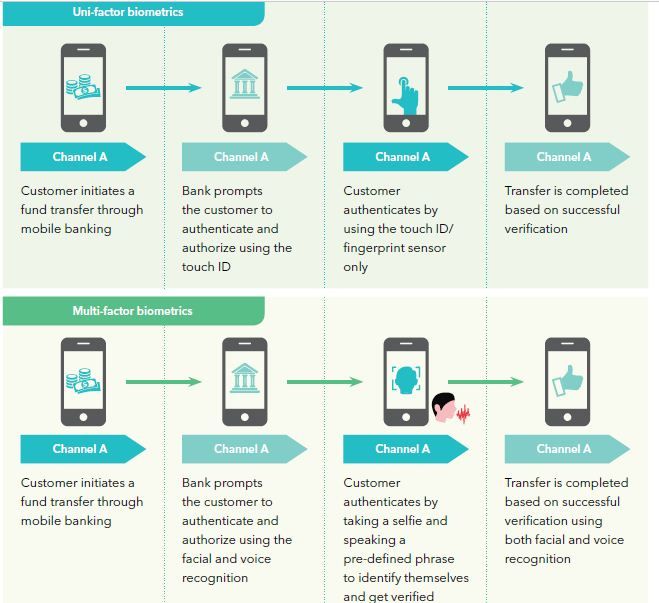

Biometrics

MadAppGang is a development company with a focus on security, and we always recommend two-factor authentication, blocking financial app functionality on jailbroken devices and more. All of which we implemented in WebMoney, a worldwide online payment system.

These security measures meet fintech compliance regulations and remain efficient and indispensable in coming years. Existing security measures can be reinforced with biometric authentication, which is swiftly becoming a gold standard. As it's almost impossible to fake fingerprints or retina patterns, biometrics adds an extra layer of security for mobile banking apps. It’s sophisticated protection against fraud that makes mobile banking more intuitive and easy-to-use.

Source: Wipro

Open banking

Open banking allows third-party Application Programming Interfaces (APIs) to access a consumer’s financial info. For customers, this means it’s easier to sign up for a new credit card, switch from one bank account to another, or connect budgeting apps to track and plan spendings. For businesses, it means an opportunity to create new services like QuickFile, an app that automates accounting for small companies.

Source: QuickFile

Open banking is one of the most discussed trends in mobile banking, but security is a concern voiced by many. The concept of third parties accessing customers’ data may seem troublesome, but data is shared only with accredited and verified third parties, and only when the customer chooses to do so. Experts note that open banking is just as safe as standard online banking.

Final thoughts

2020’s Covid-19 restrictions created a need for stable, secure and intuitive mobile banking apps. Lockdowns pushed the industry to evolve quickly and adopt cutting-edge technologies. The result is a competitive mobile banking scene where institutions without advanced mobile banking solutions are left behind.

Apps that make smart use of new technologies and tap into trends efficiently attract and retain customers by enhancing the user experience, and making it seamless and innovative.

If you want to build a mobile banking app that integrates cutting-edge mobile banking trends, contact MadAppGang today. We have the skills and know-how needed to create secure and performant fintech software that gives your business a competitive advantage, and keeps your customers happy.