How Much Does it Cost to Develop a Mobile Banking App?

Market Researcher

Almost two billion people use online banking services including apps, and the global mobile banking market is expected to reach $1.8 billion by 2026. Already in 2018, the average consumer accessed their banking app daily, and 2020 has accelerated this trend. The growing pool of Gen Z users, who are very tech-savvy and used to mobile-first services, is expected to cast traditional banking aside, but the pandemic has sped up the process due to the increased need for safe cashless payments.

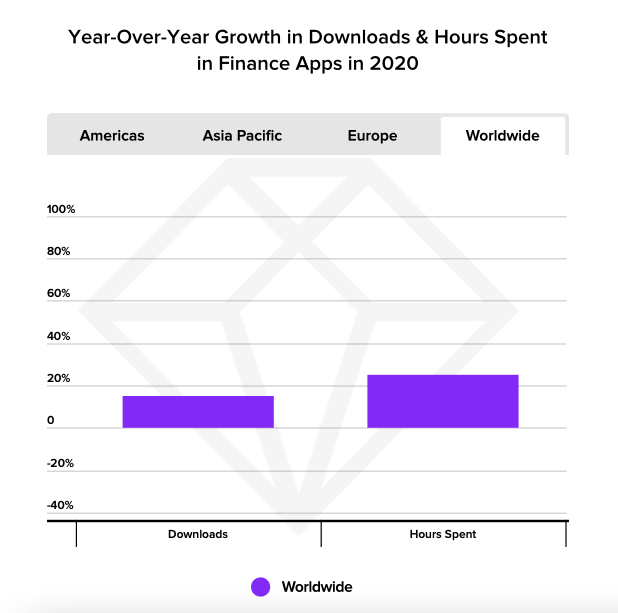

App Annie’s 2021 State Of Mobile report shows that global usage of financial apps rose by 25 per cent, reaching a growth of up to 45 per cent in some locations.

Source: App Annie

This shows a shift in financial thinking, which financial organisations should understand to attract and retain customers. It’s important to stay in tune with the market and learn what features build retention rates among users.

If you plan on building a banking app, you have to understand what technologies you need, what regulations may apply, and the scope and cost of development. In this post, we’ll explore how much it costs to develop a mobile banking app and what factors influence expenses.

Features of a mobile banking app

The cost of developing a banking app is directly linked to features and their complexity. Each function that you want to include will increase the expenses, and the more labour-intensive or technologically unique those functions are, the higher the cost.

We’ll outline some of the most common banking app features and give estimates of how much time (in sprints) goes into their development. To roughly calculate the cost, multiply the total number of hours by the rate of the engineers you hire. We’ll cover the question of developer rates later.

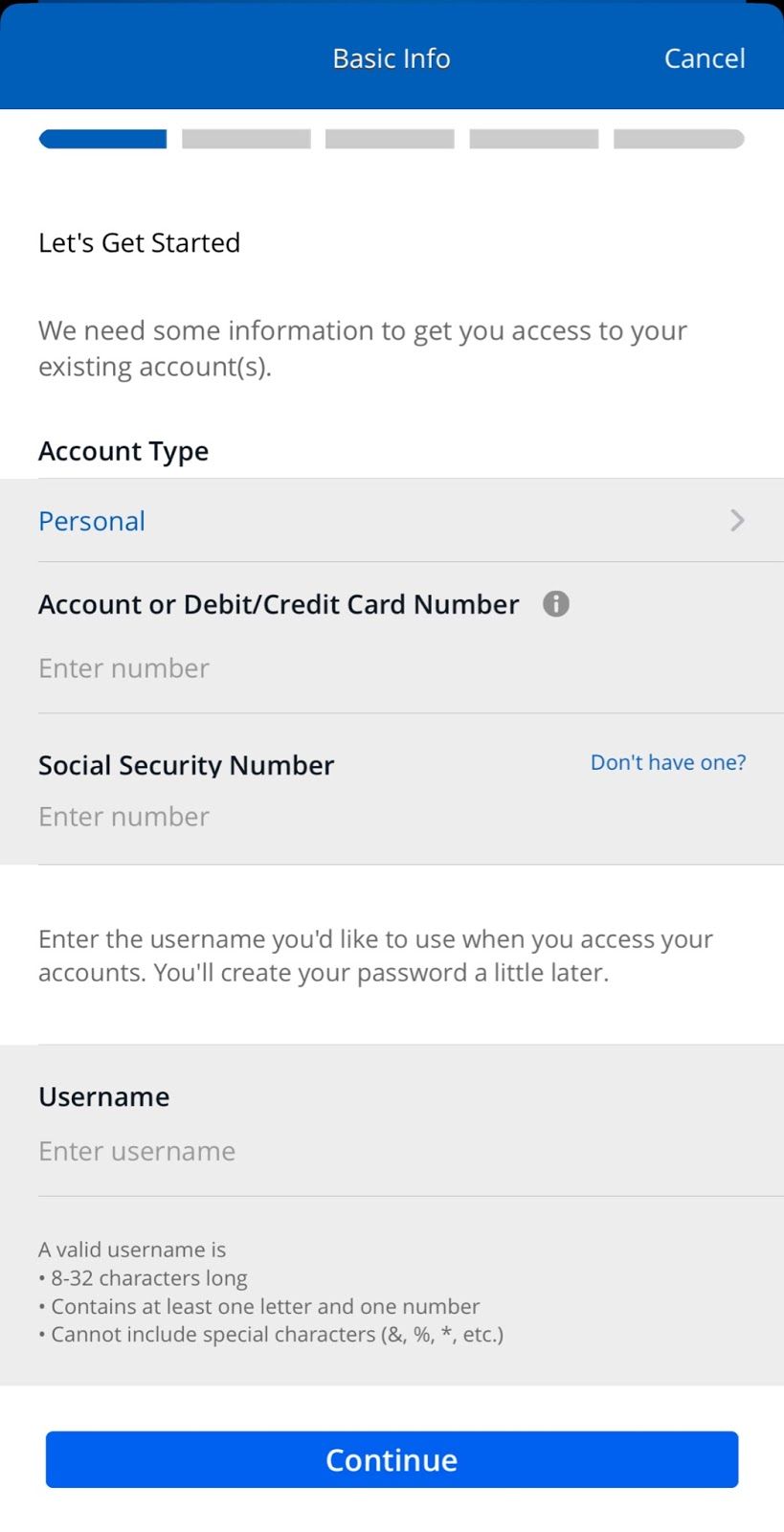

Registration

A banking app should have a clear registration and onboarding process. Users will continue with their accounts or have the option to open an account via the app. To register, they will need to provide a bank account number (if they already have one) or SSN and personal information (name, date of birth). Then, they will need to read and accept the terms and conditions and set up their app preferences.

Chase Mobile. Source: App Store

Sprint estimate (registration): 2

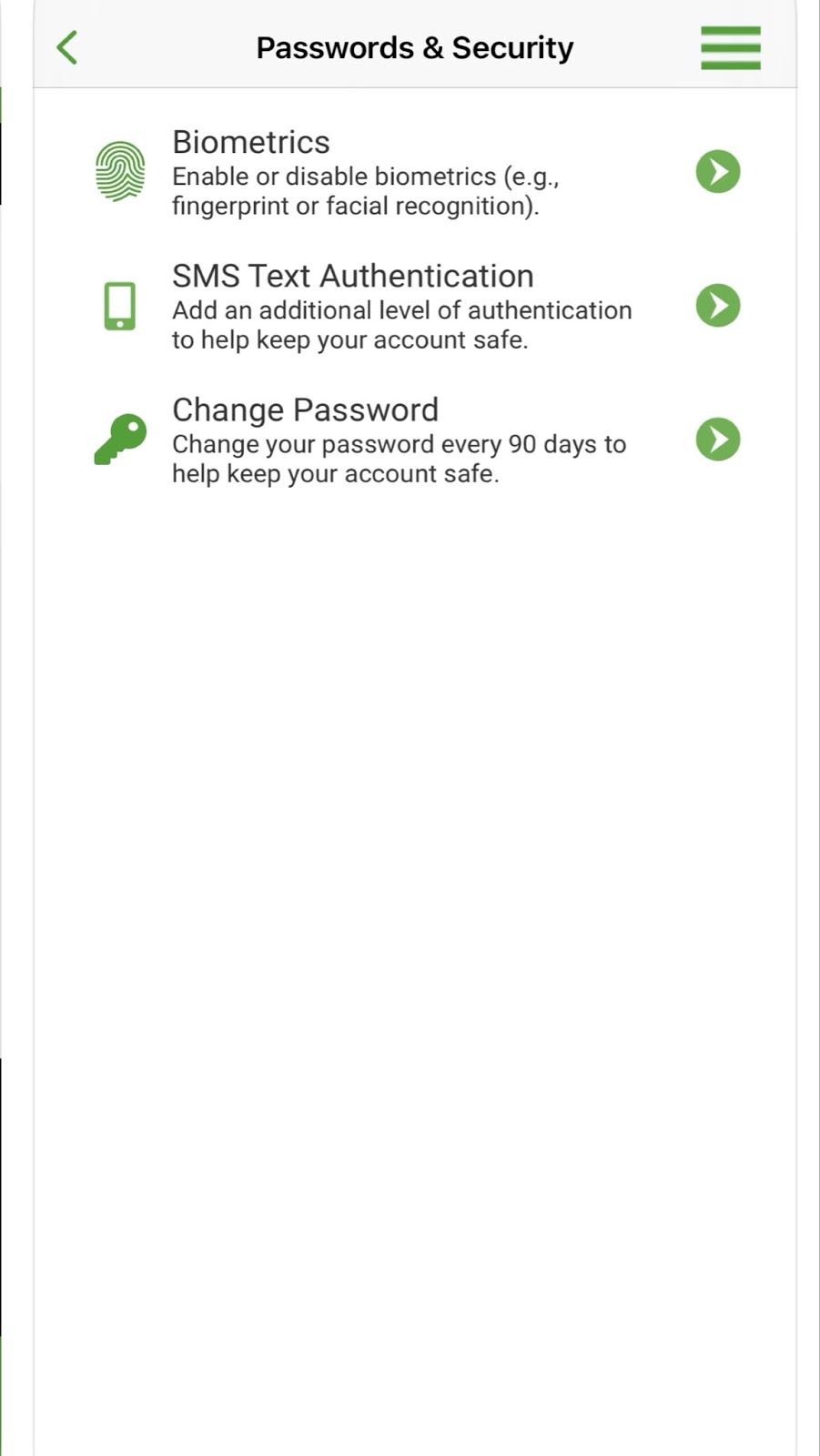

Authorisation

User sign-ins should be highly secure. You can go with PIN sign-in, fingerprint, or face recognition. Other types of biometric authentication such as voice recognition can also be integrated into banking apps. To make the app more secure, you can implement multi-factor authorisation: the most common method is to send a code via SMS and ask users to enter that code in the app.

The choice of authorisation methods in the Woodforest Mobile Banking app. Source: App Store

Sprint estimate (authorisation): 1

Including biometric authentication methods: 2

Account management

This is the essential part of any mobile banking application. Users should be able to quickly access their information and manage their bank accounts (block or reissue a card, open a new account, and similar).

Sprint estimate (available balance, account settings): 2-4

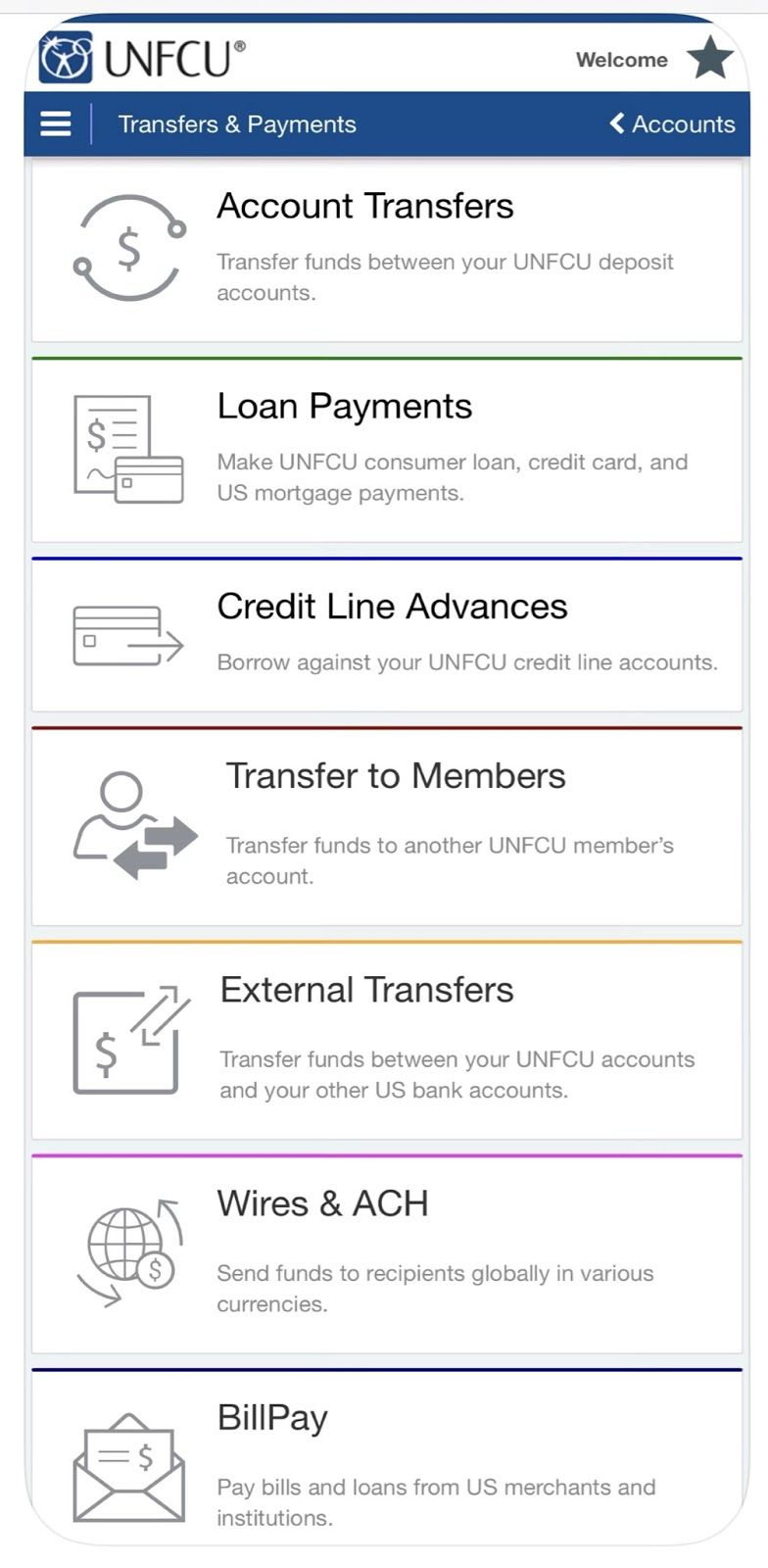

Payments

When designing payment features, you need to keep in mind all the particular transfers your users will need. It makes sense to include:

- Payment categories. It’s easier for users to make payments when they can select from clearly set out categories (peer-to-peer money transfers, utility bills, and so on).

Payment categories in the UNFCU Digital Banking app. Source: App Store

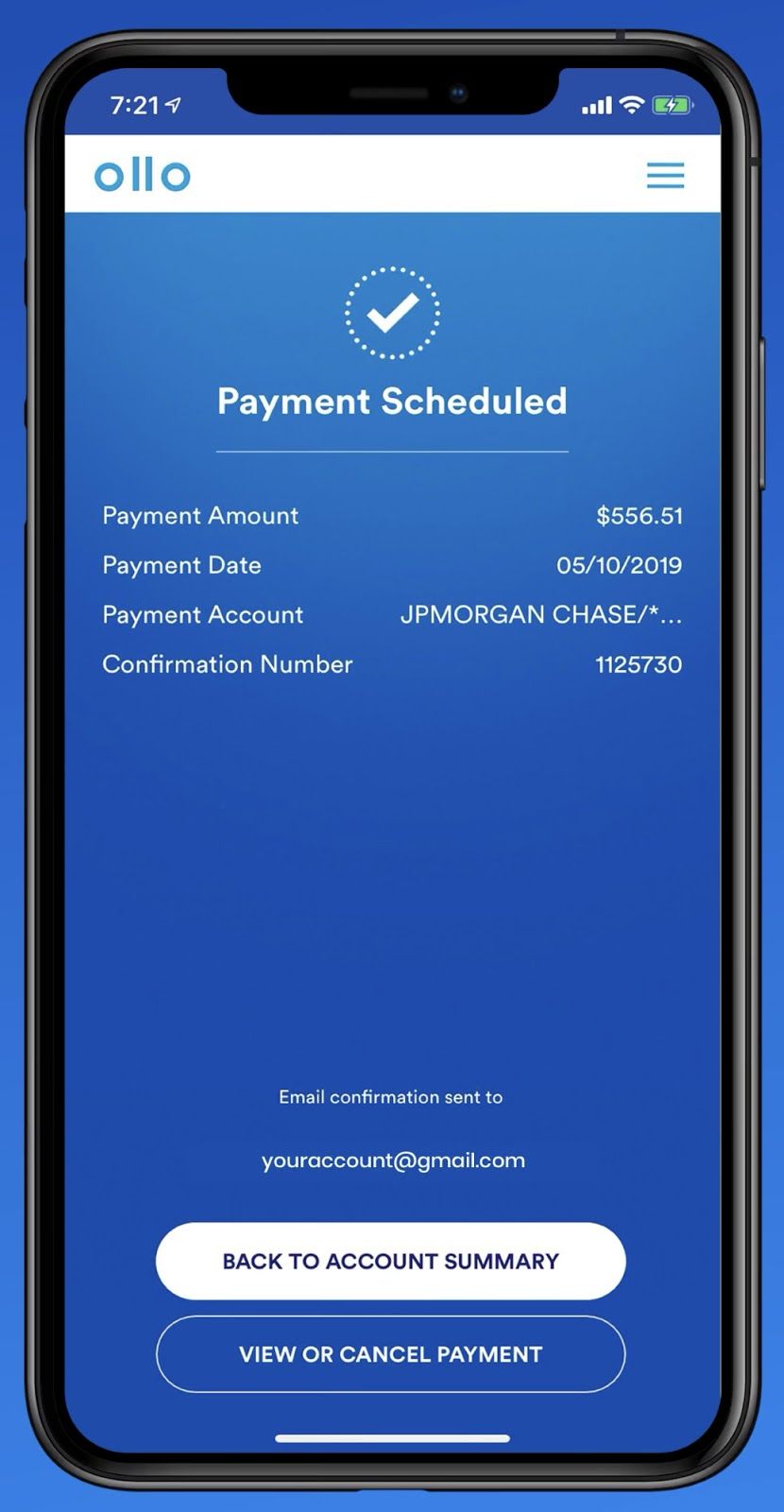

- Templates for regular payments. A lot of payments have a repetitive nature, so providing customers with templates and the option to schedule transactions in advance adds convenience.

Scheduled payments in the Ollo Credit Card app. Source: App Store

- Automated emails. Users will save time if they have the option to send receipts by email via the banking app.

Sprint estimate (payment functionalities): 4-8

Transaction history

While keeping the transaction history screen concise, you have to include a lot of useful information like the time and location of the transaction, exchange rate if the payment was made in another currency, and so on. Add an option to view transactions within a custom date range and the option to search by amount or recipient.

CFC Mobile Access. Source: App Store

Sprint estimate (transaction history): 2

Digital wallet integration

Digital wallets are gaining momentum. A recent Visa study found that 39 per cent of SMEs accept digital payments, and according to a Finder survey, 110 million US citizens, around a third of the population, have used digital wallets. Think about adding support for Google Pay, Apple Pay, Samsung Pay, Fitbit Pay, Garmin Pay, or other payment services.

Sprint estimate (Apple Pay integration): 2

Notifications

It’s important that users receive timely notifications about their accounts. Push notifications in a banking app might concern transactions, promotions, and app updates. Users should also be able to opt in and out of email alerts about account and in-app activity.

CareCredit Mobile. Source: App Store

Sprint estimate (push notifications): 2

Security measures

Security breaches and data leaks may lead to enormous financial and reputational damage, so it’s crucial to protect the information in the app. We’ve already mentioned multi-factor authentication but there are many additional aspects to consider: end-to-end encryption, hashing algorithms, AI-based fraud detection, and so on. You should search for developers who have worked with fintechs and know how to develop a secure mobile banking app.

At MadAppGang, we put our best effort into increasing cybersecurity awareness and ensuring bulletproof protection for software solutions. When working on WebMoney, we encrypted data on both the system and application levels, used a custom DNS server, and adopted other measures to protect the app from various attack types.

Sprint estimate (multi-factor authentication, data encryption): 4-6

Additional, nice-to-have app features

The above features are a must in any app handling finances. Apart from that, you can make the program more convenient with the help of advanced functionalities or third-party integrations. Naturally, you should consider any feature implementation in the context of your project’s goals and your users’ needs.

Note that to get more insights about your audience, it’s a good idea to conduct user interviews and create user flow maps to prototype everything that should be in place. This chunk of work will also take time and money, but don’t underestimate the discovery stage, as this can help you make a product that not just performs standard actions but adds value to users’ lives.

Now, let’s examine some of the above-average features that are already proving their importance in the banking and finance app development market.

Cardless ATM withdrawal

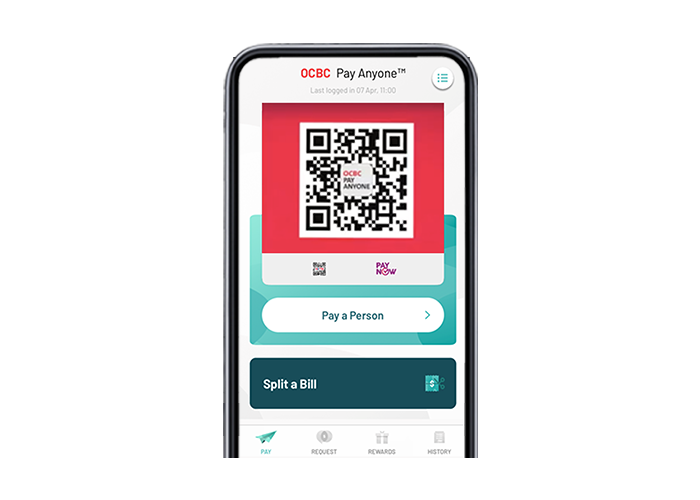

The pandemic pushed many banks to offer a card-free withdrawal option. This can be realised in several ways, for example, by having a QR code in the app to access accounts on an ATM or by adding a card to a digital wallet that’s scanned by an ATM.

A QR code with cardless cash withdrawal in the OCBC app. Source: OCBC Bank

Sprint estimate (QR code for ATM access): 2-4

Balance check without login

Some banks find it useful to provide customers with the option to check their balance on the go without logging in. Citibank’s app was the first in the US to offer this feature.

The Citi Mobile Snapshot feature. Source: Citibank

Sprint estimate (quick access to account balance): 2

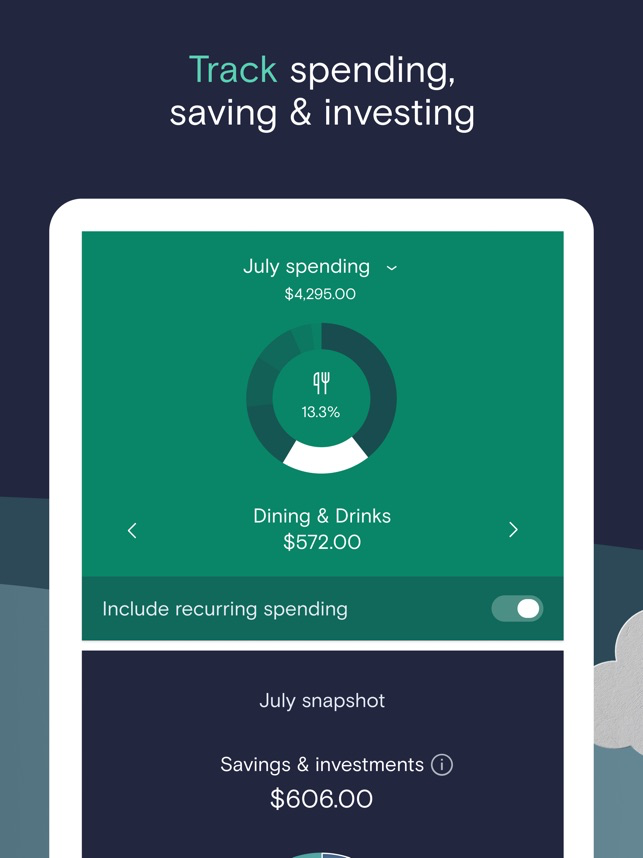

Money spending insights

There are lots of separate apps that track spending, but it has become a trend to include some kind of analytics feature in banking programmes. For example, the Marcus app features Marcus Insights, which allows users to link external accounts and track spendings, savings, and investments. The majority of people under 30 use budget apps at least once a month, so this is something worth considering.

Marcus Insights. Source: App Store

Sprint estimate (money tracker): 4-6

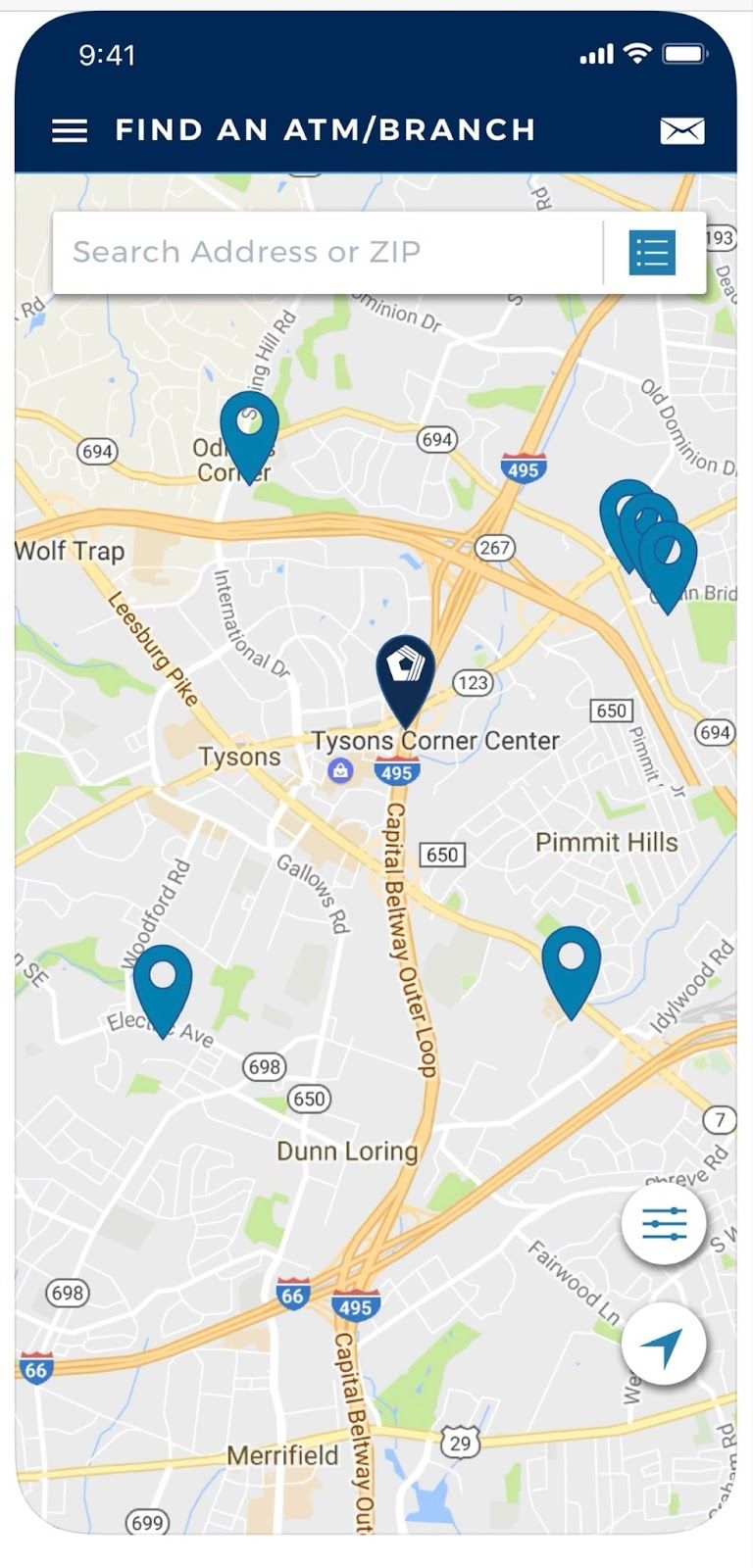

Map integration

For any financial app that supports the management of accounts opened in traditional physical banks, it makes sense to add a map with bank and ATM locations. Integrating a popular mapping SDK is a simple way to achieve this.

PenFed Mobile. Source: App Store

Sprint estimate (Google Maps SDK integration): 2

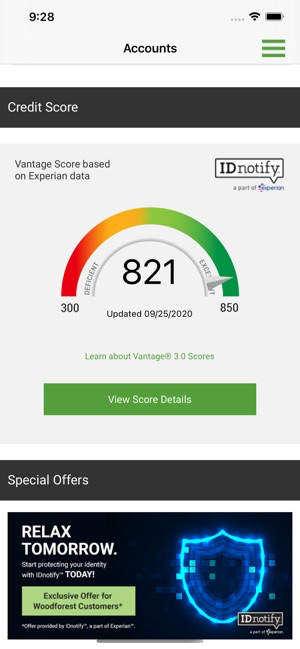

Credit score

A lot of banks are incorporating a credit score calculator into their apps. Credit scoring defines how eligible a customer is for loans and is usually based on a nationally recognised score range. In the US, it’s the FICO score that ranges from 300 to 850. Adding the possibility to check the credit score saves customers time and makes the app more informative. It’s even more convenient when the app provides details on what factors impact a credit score and how to improve scores.

Woodforest Mobile Banking. Source: App Store

Sprint estimate (credit score calculation): around 8

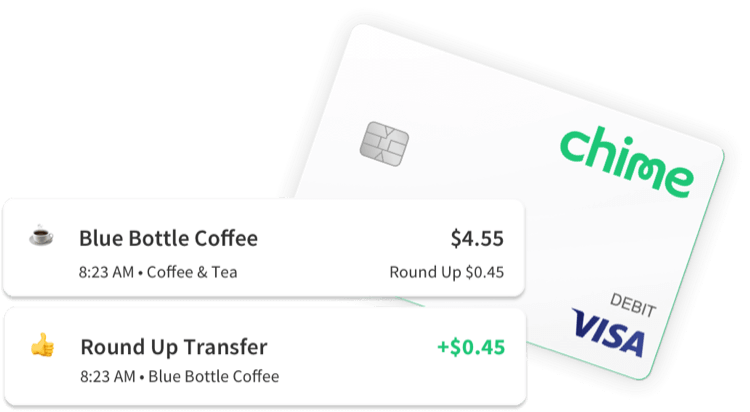

Savings automation

This is a nice-to-have feature that has proven helpful among users. For instance, Ally Bank has a Surprise Savings feature that transfers small amounts of money left in a client’s account to their savings account. Chime app offers a Save When You Spend feature that rounds up the sum of the purchase and sends the difference to a savings account.

The Save When you Spend feature. Source: Chime

Sprint estimate (savings automation): 4

Virtual assistance

Functionalities activated and controlled by voice are coming to the fore in many industries, and banking is no exception. For example, the Royal Bank of Canada and UK bank Barclays have added Siri support, enabling users to make payments using just their voice.

Sprint estimate (Siri integration): 2

Some banks go to even greater lengths and introduce their own virtual assistants. For instance, the Bank of America features Erica, that not only helps make payments but also can provide information on spending tendencies. The US Bank Smart Assistant works in a similar fashion, and these advancements make banking apps more competitive and popular with users.

Virtual assistive technologies are not exclusively associated with voice commands. Banking apps also design assistants that function similarly to chatbots. For example, Capital One’s Eno supports dozens of typing shortcuts that help manage bank accounts and perform financial operations.

Chatting with Capital One’s virtual assistant Eno. Source: VentureBeat

This is an area for endless innovation and improvement — AI-based technologies like deep learning are already used to step up the quality of Siri and Amazon Alexa, and can power mobile banking apps as well. But it will come at an additional cost, and you can only get a rough estimate after you discuss your particular project with a development team.

This is not an exhaustive list of features that you can include. For some banking apps, it will be helpful to add QR code scanning and image recognition, a split bills function, cashback systems, chatbots, and others. The most important thing is building the app’s capacities according to users’ needs — don’t go for innovative features just for the sake of innovation or trend.

The more you move toward innovative technologies and additional integrations, the higher the final cost range will be. Although, there might be situations when it’s possible to develop a banking app with low-code and no-code solutions to cut expenses and hasten the time to market. For instance, the Rabobank case shows a 50 per cent cost reduction with no compromise to scale: its online portal, which is made with low-code and no-code tools, handles over 500,000 customers. If it makes sense for your project, we will guide you through cost-cutting low-code options for developing certain app components.

For now, let’s move on to the cost of hiring developers and the hidden expenses to consider.

Developer rates

The set of features detailed above is the first significant factor in app development costs. The second is the rates of the professionals hired, including developers, testing engineers, designers, software architects, project managers, and others. Those rates depend on the following:

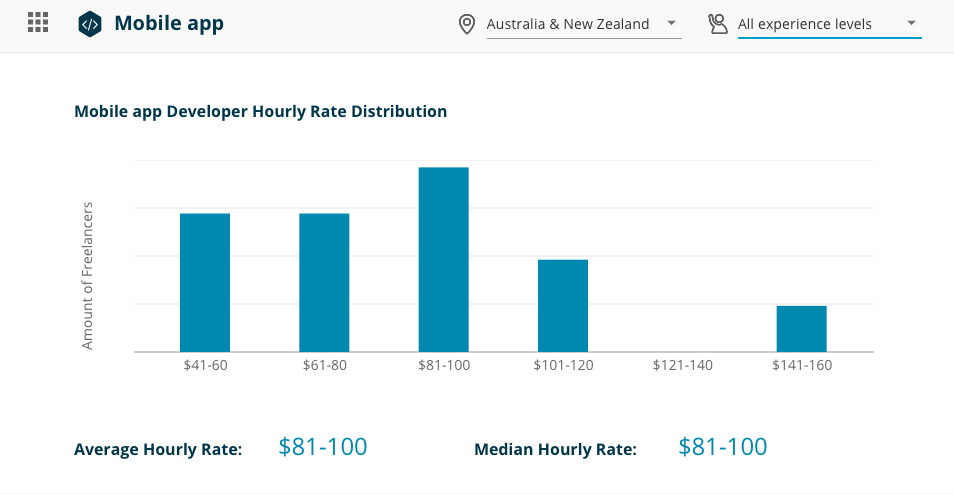

- Location. IT specialists from Northern America and Eastern Europe, for example, charge a drastically different amount per hour. According to the 2020 freelancer survey, the average global hourly rate of a mobile app developer is $61-80. If you’re looking for Australia-based engineers, the average rate is $81-100.

Source: Codementor

- Experience. As a developer’s leve (Junior, Middle, Senior) and years of relevant experience increase, so too does their hourly rate. Entry-level app developers in the US start from $25 per hour, while Seniors charge up to $75 per hour. Note that these rates concern individual professionals who are not employed by companies: in the latter case, costs will be higher because of additional corporate expenses (office rent, employee insurance, etc.).

- Tech stack. On average, the cost of iOS and Android app developers are similar, but there might be nuances when it comes to specific technologies and frameworks that influence developer rates.

- Type of employment. Hiring freelance developers and other IT specialists may cost less (a comparison of full-time and freelance developer rates shows that the latter is up to 50 per cent less expensive) however, it’s always best to find a development company that will provide you with a dedicated team to cover all your needs. When you discuss your idea with an experienced software architect and then your project is handed to developers, testers, and designers who work in sync, the chances of getting a successful product are significantly higher.

Note that if you hire individual banking app developers, you will have to hire designers separately, which may be cost-saving initially but leads to a longer development time as the disconnect between professionals becomes apparent. The knock-on is more adjustments, more remakings, more time, and ultimately, more expenditure. In contrast, when the team building the app’s features is in direct cooperation with the team designing the user interfaces, it’s easier and faster to make a successful product.

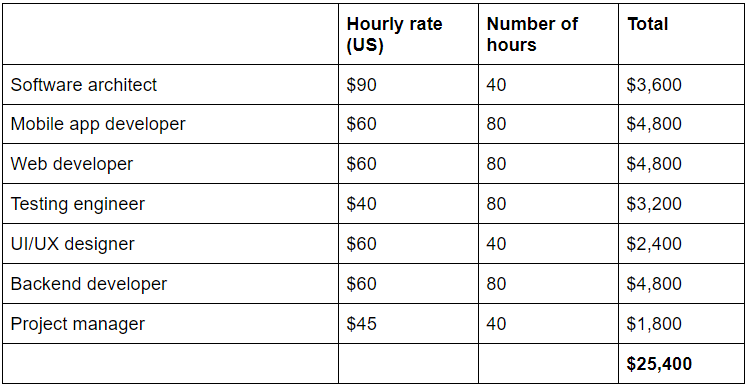

Here’s what a typical mobile banking app development team consists of and what one sprint (two-week iteration) can cost:

This is a rough estimation of a single development sprint. Naturally, the higher the project’s complexity, the more team members are required and the more expensive the banking mobile app development will be. To understand an approximate cost, weigh up different features and consider how long it will take to build these. Check out our sprint estimates given for each mentioned feature.

Other expenses

When you find a perfect team that works in tune with you and set up a budget for them, this is not your final banking app development cost. Here’s what you also need to consider:

- Regulatory assistance. Financial apps contain sensitive data and are, therefore, heavily regulated. Fintech regulations are fragmented and the responsibility for oversight is distributed across many organisations. A development team with fintech expertise will know the basics but it won’t hurt to have qualified compliance assistance to make sure that the app is properly protected and won’t compromise user data.

- App release. Marketplaces like Google Play and Apple Store charge one-time or annual commissions and also have fees for in-app purchases. In the context of the full project cost, it doesn’t seem significant but should still be considered. App rejections might make the process harder and drive higher expenses.

- Servers and data storage. The storage of data requires constant maintenance, which can take up to 20 per cent of all banking app development expenses per year.

- Third-party services. Some of the integrations in payment apps charge a monthly or yearly fee. For example, industry-specific APIs like Plaid can cost more than $500 per month.

- IT support. A mobile app is never “done” as you will eventually need to fix bugs and publish updates. It’s estimated that bugs take over 10 per cent of the total development budget annually.

Final thoughts

There’s no average cost of mobile app development as it ranges from $10,000 to $1,000,000+. From our experience, financial apps are complex and challenging solutions that cost over $500,000, but it all depends on the features, integrations, and technologies involved.

You can’t get an accurate development cost estimate before you discuss your particular project with a seasoned team. Reach out to us to learn more about banking app development cost in the context of your ideas and business goals.