How to Start a Fintech Company in 7 Steps

Market Researcher

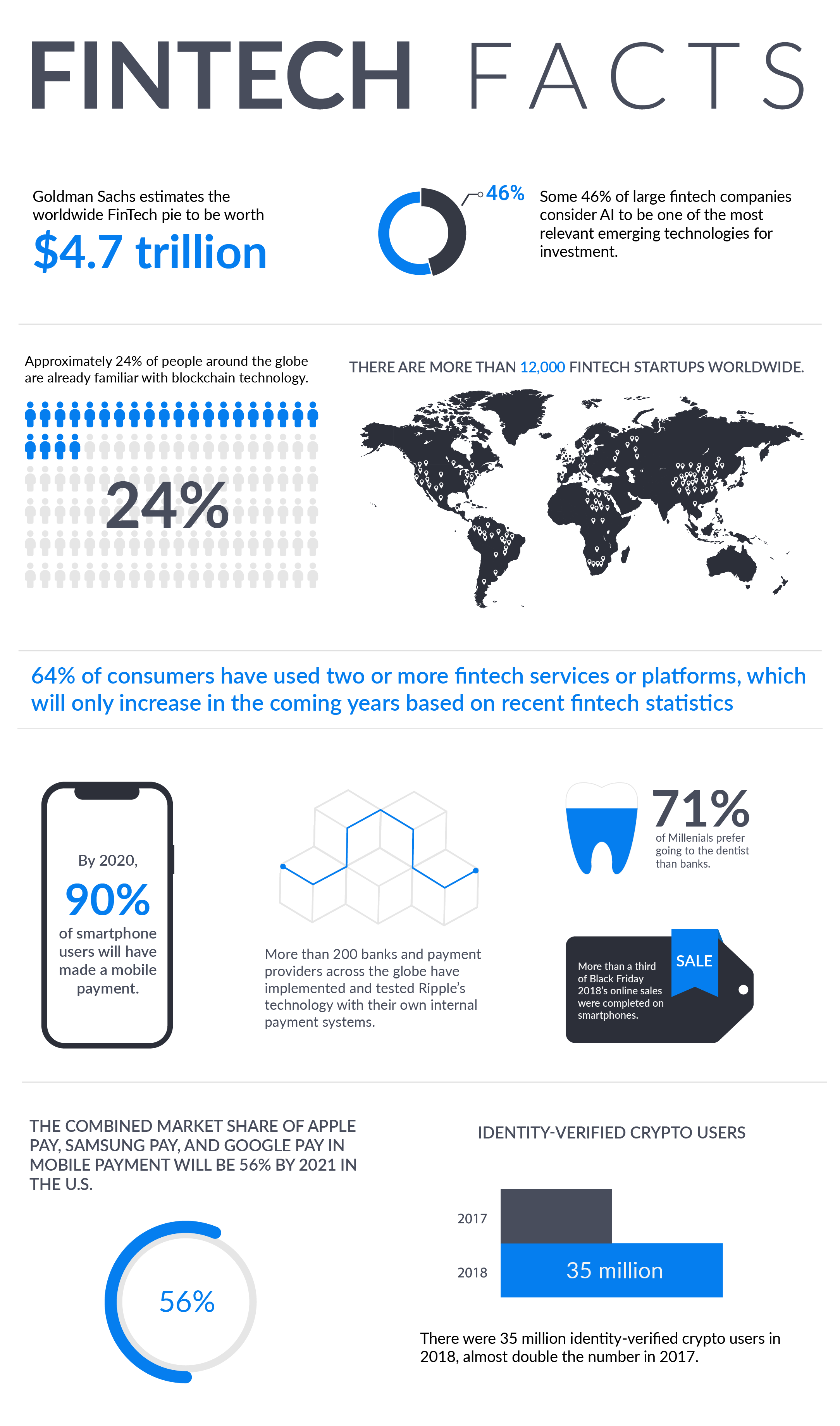

In 2019, the fintech market was valued at a substantial US$111.2 billion, and by 2025, it’s expected to hit US$191.8 billion with steady growth in between. And a considerable share of the market is still up for grabs; EY’s 2019 Global Fintech Adoption Index revealed that globally, consumer adoption of fintech was still low at only 64%.

Suffice it to say, starting a fintech company in 2021 can be a very promising and profitable enterprise. But the market is huge, and so is the competition. So how do you create a fintech startup that has a chance of standing alongside giants such as Revolut or PayPal?

Source: Gatehub

Theodore Roosevelt once said "believe you can and you're halfway there" — have an idea, believe in it, and you're already part way towards achievement.

If you have a novel idea for a fintech solution, but you’re not quite sure how to take it further, you’re in the right place. MadAppGang has created a seven-step guide on how to build a fintech start-up based on our experience with successful financial and e-commerce projects. Think of it as a cheat sheet to get you started on everything fintech.

First, though, let's take a closer look at the various fintech niches including mobile banking, personal finance, trading apps, and more. Specifically, what are these products, what value do they offer users, and are they profitable?

Below is an overview of most popular financial technology start-ups and types.

Market overview: The main fintech platform types

Before you build your start-up, choose the type of fintech software as there are several options, from digital banking to investment. Narrowing your niche allows you to build a clearer plan and explore the required technology for your fintech solution in greater detail. Here are the major types of fintech software you could develop:

Web and mobile digital payment apps

Today’s mobile payment solutions were kickstarted with the introduction of Apple Pay in 2014. The category includes such services as e-wallets, payment processors, and cashless payment apps that allow users to store funds, pay for various services in different countries, and much more. They also make transferring money easier, making these services highly popular worldwide.

The digital payment app market is quite promising. Research shows that the fintech payment market is expected to expand further too, driven by initiatives to promote digital payments, m-commerce growth, increased e-commerce sales, and huge internet penetration. The global digital payments market is projected to grow from US$79.3 billion in 2020 to US$154.1 billion by 2025.

Keep in mind that the rivalry in this sector is fierce. Once you launch your fintech start-up, you'll have to compete with popular and established popular apps such as PayPal, Apple Pay, Google Pay, and Venmo to name just a few. To make a good start in this field, it makes sense to study the competitors inside-out, and ideally find a gap in the market you can fill with a unique service.

Source: Dribbble

Mobile banking apps

Mobile banking apps bring a bank to your pocket, so you’re not limited by working hours and can access your account anytime. These innovative banking products allow users to conduct financial transactions via mobile devices. Nowadays, many traditional banks offer a mobile app, but often, those apps are very basic and lack advanced services such as QR-code payments or Google/Apple Pay integration.

Whether you run a traditional bank or are planning a start-up, consider making your mobile banking app as advanced as possible. User comfort is as important as security and reliability. Take neobanks (banks that only operate online) such as N26, MercuryBiz, or Revolut as an example. Let customers open bank accounts remotely, get cashback rewards, buy goods and pay for services directly from your banking app, and more.

Source: Revolut

The competition is stiff in this sector, too, although there are still service gaps that your unique product can cover. Taking security to the next level or offering extra services like automatic tax calculations can net you a piece of a market expected to reach US$1.82 billion by 2026, according to Allied Market Research.

Digital lending apps

Digital lending apps are a type of financial technology product that offer loans online. Most lending apps are automated platforms adapted for speedy credit analysis, loan decisions, and administration. It's a very comfortable service for users as the entire loan cycle occurs online, and no awkward bank visits are required.

Some lending platforms are simple apps or websites while others are AI-powered products that streamline interactions between lenders and borrowers. Dave and Earnin are basic platforms that lend money instantly without any credit score analysis. Blend, Better, Open Lending and SALT Lending are good examples of advanced lending platforms based on the newest technologies.

Source: Lilian Telez

Another prime example in this niche is the Bond Street app, which uses data-driven algorithms that analyse profitability and other factors pertaining to small businesses after personalised loans. In a word, it’s an excellent solution to take inspiration from. Your fintech start-up shouldn’t provide less, otherwise, you’ll have nothing to beat the competitors.

Your investments in an AI-powered platform will pay off. This is a growing and thus welcoming market. By 2028, the global digital lending platform market is expected to reach US$27.07 billion, according to Verified Market Research. If you release a top-notch, innovative service, there’s every chance of getting a slice of the pie.

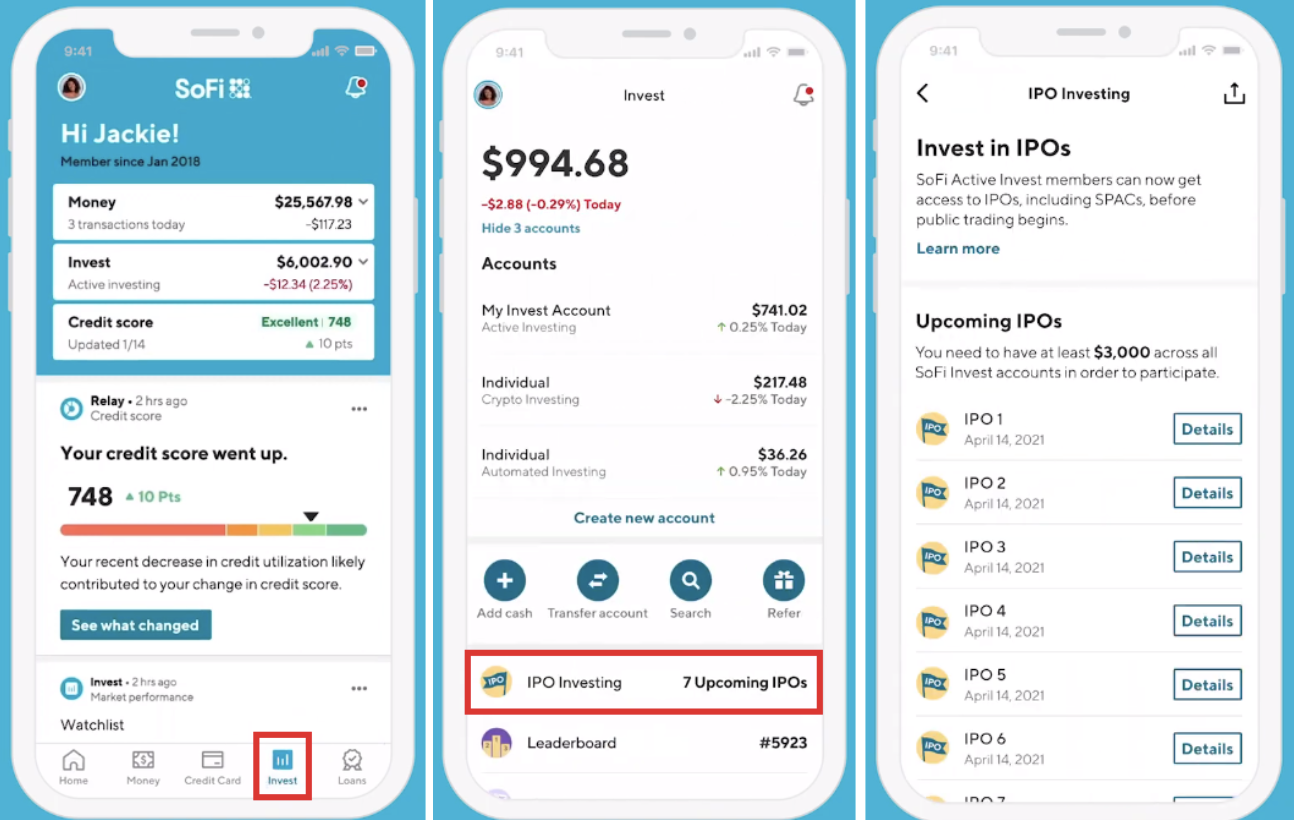

Trading apps

A stock trading app is an application that lets you manage your portfolio and trade stocks on the go using a mobile device. These platforms make trading affordable and understandable for everyone. Along with stock trading, trading apps offer users information on investing, real-time market data, analyst ratings, news, and even advisory services (human or AI-powered). Some investing apps, including SoFi, enable crypto trading and crypto exchange as well.

Source: SoFi

According to Verified Market Research, the online trading platform market was worth US$13.1 billion in 2019 and is projected to hit US$18.3 Billion by 2027. The growth of digitalisation globally and increased awareness of online trading and investment options are the major drivers behind the market’s rise.

As the market expects lots of inexperienced players (your potential users), it's a good idea to make your investment platform as easy to use as possible. Simplicity, a user-friendly design, together with detailed guides and advanced features like robo-advisors are the key to success — and beating the competitors.

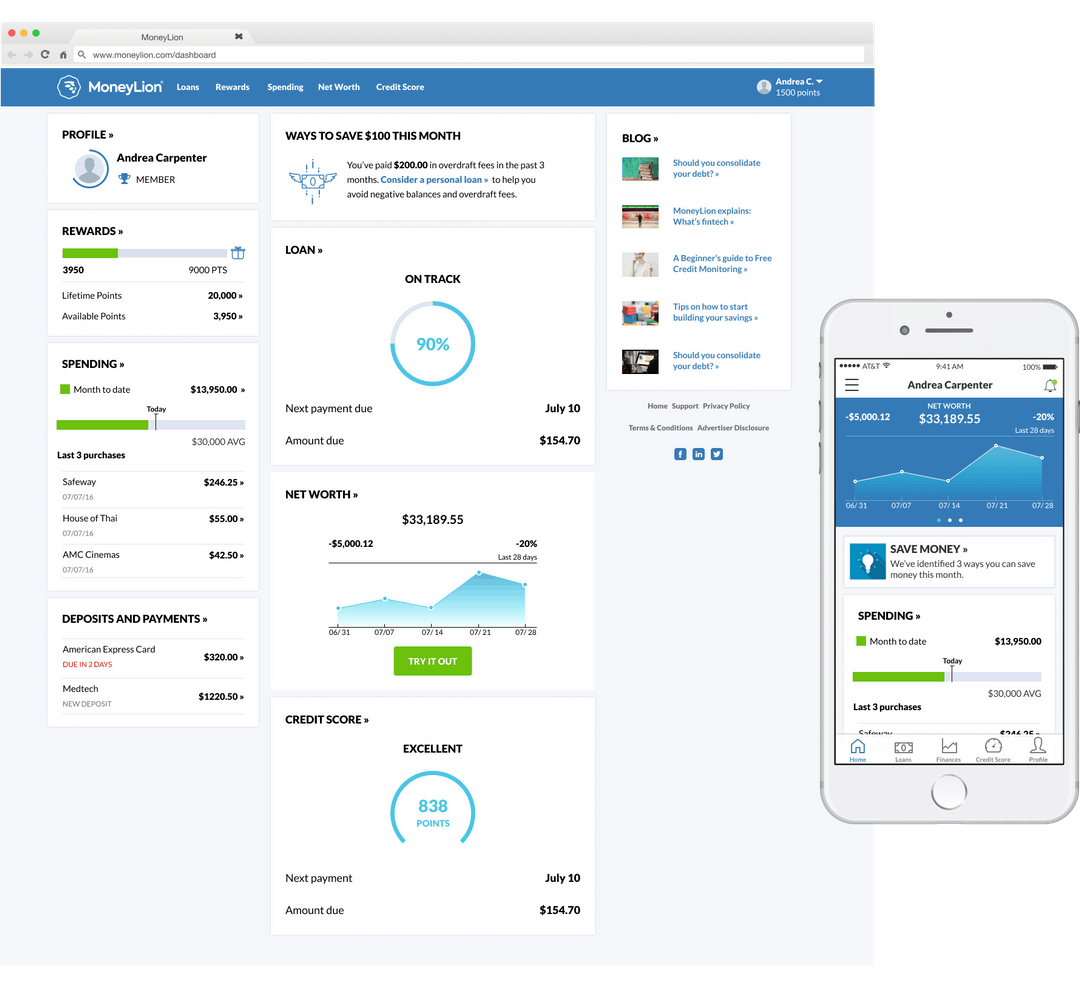

Personal finance apps

If you’re starting a fintech company for the first time, personal finance apps are an excellent place to begin as most do not require as many permissions and licences as banking apps, for example. Besides, it requires less initial investment, unlike banking platforms, building a personal finance company requires less capital expenditure.

Source: Dribbble

Usually, personal finance apps don't process payments. Instead, they help users manage their finances by tracking spending, saving, investments, bill payments and credit score changes. The PocketGuard, YNAB and Mint apps are classic examples of personal finance platforms.

The personal finance software market is estimated to rise from US$1.02 billion in 2019 to US$1.57 billion by 202, and demand for this type of finance app will only rise accordingly.

How to build a fintech start-up in 7 steps

Step #1 Learn about fintech regulations in your country

Learn more about the local rules and regulations for fintech and your company’s planned activities in detail. Every country has different regulations, and in some cases, it can be tricky. For example, in the US, fintech businesses are not subject to a specific regulatory framework, but depending on the activities of your company, it may be subject to various federal and state regulations such as Anti-Money Laundering laws and the Bank Secrecy Act.

Failure to comply with local laws and regulations can result in hefty fines and legal action. Partnering with a software development company that knows fintech and prioritises data security is essential.

Step #2 Establish a vision for your project

Outline your product’s main tasks: what problems it will solve for users, and what core features should it have? For example, for a budgeting app, the list of key features should include: registration, login and authorisation, personal profile with a settings section, spending and receipt tracking, and data analysis and reporting. For a mobile payment app, the list of features is similar, but in this case, you also should include the ability to send and receive payments and point of sale (POS) integrations.

Step #3 Analyse the market and find your competitive advantage

Learn more about your competitors. Understanding what is already provided by others allows you to discover untapped opportunities or needs. In addition, your service should cover as many user needs as possible and go above and beyond existing solutions, this will become your competitive advantage. Alternatively, your solution might just enrich an existing product or service already on the market. Both variants are fine, as long as you achieve a competitive edge to help your fintech company thrive and succeed.

Step #4 Think about your users

The user experience is as important as security. You should provide a seamless user experience at every stage of a user's journey, from signing up to completing a task such as connecting a bank card or getting a monthly spending report. Intuitive design, easy security checks like Face ID, and a competent support service are key. Hiring a business analyst is a good idea too as they can help identify your target audience, define user roles on the platform, and make a list of features around user needs.

Step #5 Choose a monetization model for your fintech start-up

There are many ways to make your company profitable. To choose the right monetization strategy, first, you need to decide who pays — customers, third-party sellers, or third-party beneficiaries. If you plan to get revenue from customers (the most widespread way to monetize fintech products), your options are subscription or transaction fees. If you plan to make your app free for users, though, you have two other options:

- Find third-party sellers who will pay for referrals and/or advertising. For instance, Credit Karma's algorithms pick and show relevant ads to the app's 100 million users, and get paid when they follow these recommendations.

- Choose third-party beneficiaries, that is, outside organisations your company generates direct and indirect income for and receives payments from. For example, whenever a Chime customer pays for a purchase with a Visa debit card, Visa charges the trader an interchange fee (IRF) and later pays Chime a portion.

Step #6 Build a Minimum Viable Product (MVP)

An MVP is a basic version of a product with essential features that you can show to customers. This is an important step in building a fintech start-up as it allows you to gather analytical data about your app and get feedback from real customers. The data and customer reviews will help you understand what should be improved in your product. Also, it's a good way to know what core and advanced features are missing.

Step #7 Test and improve your product

Test your MVP, get user feedback and analyse the data. Deep analysis will help you decide what exactly you need to include in the final product, be it to add advanced features, strengthen security, change design or navigation, and so on. Then test the product again. Constantly maintain, improve and update it. Otherwise, you risk losing some of your customers to your competition.

Source: Anand Thaker

Mistakes to avoid when creating a fintech startup

Like in all industries, financial technology startups have challenges and risks. Building a fintech start-up is not always a piece of cake. Though, if you work hard, comply with all the regulations in your country, think of your customers first, and avoid common mistakes, creating a fintech company is much easier. Let's take a closer look at the mistakes to avoid while planning and creating your financial technology project.

Mistake #1 Not addressing the user's pain points

Pain points are problems that prospective customers experience during their customer journey. A successful product covers users' needs and resolves pain points. For example, if users struggle with a rival product’s complicated interface, make your app simple and intuitive. Conduct thorough research on your competitors, study customer reviews, and you'll see which problems you can resolve with your product.

Mistake #2 Not making security a top priority

As you are creating a financial start-up, remember that you have to comply with local government regulations and, by extension, show users that your product is completely safe. Based on our experience building fintech platforms (for instance, Webmoney), MadAppGang recommends that you follow mainstream security trends but also introduce the following: two-factor authentication and/or biometric security measures, dynamic CVV2 codes, and registration via phone number.

Mistake #3 Inability to build a good team

It's easy to avoid this mistake if you already have a team of app developers and designers in your company. If not, you have three options to find specialists. First, you can build this team within the company. This is the most traditional, yet expensive and time-consuming path.

Second, you can look for freelancers, which may be cheaper but it’s still time-consuming and working with a team of specialists who have never worked together before can quickly turn into an exercise in futility. Plus, this option offers no guarantees that you'll find specialists quickly, or meet your development deadlines.

The third option is to hire an experienced development company like MadAppGang. In this case, you just need to share your start-up idea. All the tech stuff is on us. We'll help you plan your project, calculate the cost, and then design, develop and thoroughly test your fintech platform. As a result, you'll get an advanced, secure, user-friendly fintech app that brings value to your users and your business. And just as importantly, you'll be able to bring your product to the market faster as you won’t spend years building the right crew.

Summing up

Fintech is a huge market, and as it’s still growing, there’s every chance for new fintech unicorns to make a mark. Meanwhile, the competition is almost as impressive as the size of the market.

To get a share, you need a smart strategy and a robust development plan. But first, you need to choose your niche wisely according to your starting capital and the level of effort you want to exert on bureaucracy. From this point of view, creating a banking app is much harder and more expensive than creating a budgeting app, for instance.

Once you pick a niche, analyse the market thoroughly to identify the gaps that remain unmet by your rivals, and, with that knowledge, make a list of features for your product. Decide how you're going to make money with your fintech start-up, and entrust your MVP to a reliable team of professionals like MapAppGang. You can trust us to build your Android, iOS or web fintech platform, and provide you with essential information and updates at every stage of your project. Contact us and let’s take your fintech idea from conception to realisation.