Why is Fintech Growing? 4 Drivers Powering the Industry

Market Researcher

For more than a decade, the fintech industry has been growing. It has reshaped how we think of payments and brought new financial service products to the market year or year. But is fintech still growing, or is the bloom now off the rose and market opportunities for newcomers are limited?

MadAppGang has worked in fintech since its early days, for example, we worked on Webmoney, a payment platform that launched in 1998 now has over 41 million accounts worldwide. We want to share some of our observations and research on fintech. Here we overview why fintech is growing, how big the market is, and where to look for fintech business opportunities today.

How big is the fintech market?

In 2019, the global fintech market was valued at US$111 million and is expected to reach US$158 million by 2023 and US$325 million by 2030. However, some experts predict an even bigger rise in the fintech market in the next decade, as evidenced by the current surge in fintech funding.

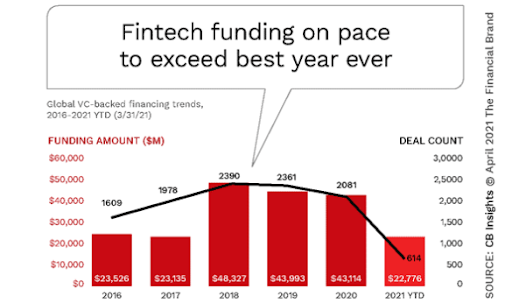

According to a CB Insights report, fintech funding is not just having a moment, it's experiencing historical record investments for "mega-rounds", in which fintechs raise more than US$100 million. If the fourth quarter of 2020 saw 30 fintech investments worth nine figures, the first quarter of 2021 is already far ahead with its US$228 million funding surge.

In 2022, fintech investment growth will accelerate and is expected to reach US$310 million. And that’s during a dramatic fall in investments caused by Covid-19 lockdowns and restrictions. The pandemic had a negative impact on most industries, but not fintech.

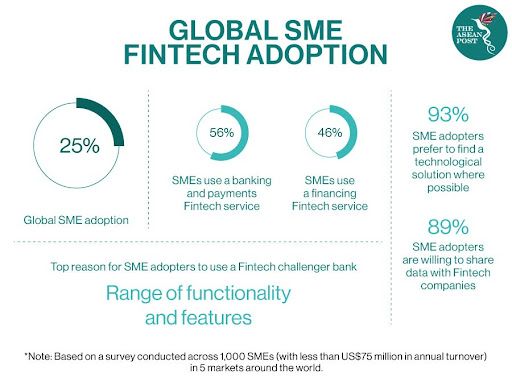

Covid-19 lockdowns saw an increased number of customers use fintech services instead of traditional banking, insurance and lending. In 2021 three out of four consumers worldwide use fintech apps to transfer money. For small and medium-sized enterprises (SMEs), today’s fintech adoption rate is at 25% and is projected to rise as high as 64% within the next few years.

The four pillars of fintech’s growth

A glance at the fintech market overview is enough to understand that the industry is booming, and is set to continue doing so. But why is fintech growing at this pace? Several key factors, from better customer service to compliance regulations, are fueling its growth. Let's take a closer look at each factor.

Technology

Technology is the main reason behind the growth of fintech. Because it operates almost exclusively in a virtual realm, it has transformed how financial services function, now almost unrecognisable from a decade ago. Machines and algorithms allowed us to automate processes that were previously performed by humans, and a whole, technology made fintechs a cut above traditional financial institutions in several regards:

- More productive – Not only does automation mean faster routine operations, but also frees staff time to focus on strategy, innovation, and other challenging tasks. The result is increased productivity.

- Accessible to anyone – By offering a broad range of financial services online and via apps, fintechs removed intermediaries such as brokers and bank managers, giving everyone direct access to services and information.

- Cheaper – Technology allowed fintechs to hire fewer employees while staying at a very high productivity level, and to save on brick and mortar offices. Savings on staffing and local branches can translate into reduced service fees, making fintech products attractive to a large audience.

Regulations

Broadly speaking, regulations can make entrepreneurship more challenging. Even though the financial technology industry is subject to regulatory obligations, many of these are not as rigid as the frameworks fully licensed banks are obliged to meet. Hence, financial technology companies can launch new financial products with greater agility.

Moreover, many governments actively encourage digital banking. For example, in 2016, the UK Competition and Markets Authority ordered nine of the country’s largest banks to grant licensed startups access to their transaction data. This helped pave the way for other fintechs to emerge and offer customers new ways to manage their finances via smartphone.

Nowadays, the UK leads on fintech internationally, making up around 10% of the global market. However, the country doesn't rest on its laurels. To reduce the burden of regulatory reports for fintechs, the UK's Financial Conduct Authority (FCA) replaced its current Gabriel reporting system with RegData, a new platform that makes submitting data easier as it’s more flexible.

Customer Expectations

In the beginning, financial technology companies engendered changes to customer expectations. After the 2008 crisis, when customers lost their trust in established financial institutions, fintech companies became even more attractive with their lower fees and charges, but also faster services and greater accessibility.

Now, a shift has occurred and customers are changing the financial industry through their expectations. Over the past decade, people became accustomed to an enhanced customer experience and greater convenience across the board — tailored offers and same-day retail deliveries, for instance. An average banking customer expects the same from the financial sector. And unlike traditional banks, fintechs are more flexible and better able to meet customer needs.

In addition, Covid-19 accelerated fintech’s adoption. The Swiss Finance Institute reported that fintech app download rates increased from 29.2% to 32.8% during pandemic lockdowns. Traditional banks were not prepared to conduct most banking operations remotely, so even hesitant customers turned to fintechs to manage their finances.

Maturing

The last, but not least, reason why fintech is growing is industry evolution. A new phase in the development of fintech is upon us. The financial technology sector matured as companies became more sophisticated and gained greater access to capital, they then scaled and reinvented banking products and services.

As an example, Zopa, the pioneering British peer-to-peer lender (founded in 2005), has now become a bank. Another fintech unicorn, Revolut, is operating as a bank in some EU countries and submitted its application for a UK banking licence. As it still offers crypto services, Revolut remains a fintech, but it will gains trust among consumers if it secures a banking license.

Source: Revolut

If Revolut is licensed, its British customers will finally be eligible for the Financial Services Compensation Scheme (FSCS), which guarantees Revolut deposits up to £85,000 per person safety. That’s a boost that will make Revolut an incumbent rather than a fintech unicorn; it will evolve even more as it gains more customers and funding.

Where to find business opportunities in fintech

The financial services market is growing, and, as we've already discussed, there are four good reasons for that. At the moment, it looks like fintech is somewhere near its peak, but some experts state that the market is only 1% complete, meaning there are opportunities aplenty. The question is how to find the opportunities fintech’s growth offers.

Experts say that different countries offer different prospects. For example, in the UK the most crowded fintech niche is retail banking and SME, with lots of customers but low value-per-customer (VPC). Meanwhile, the niches with a lower number of customers but a higher VPC, such as fintech products for medium and large enterprises, are largely untapped.

US fintechs, meanwhile, are mostly concentrated on wealth (investment apps, personal finance manager apps) and retail banking niches. The SME niche, unlike the UK market, is not crowded and is still very welcoming to newcomers.

Source: The Asean Post

The fintech suppliers market promises a bright future for entrepreneurs on both sides of the pond. You could start a company to provide data for Know Your Customer (KYC) purposes like LexisNexis and DueDil. Or your business could help bigger fintechs with staffing needs. In the supplier landscape, it’s not necessary to be a pure fintech company to tap into the huge financial technology market; all you need is a valuable service.

Final word

No matter how you enter the fintech market, you'll need a solid technology-based product. Instead of looking for freelancers or building an expensive in-house team of developers, let MadAppGang do the work for you. Let our experts handle all the technical work while you focus on developing and improving your business idea.

MadAppGang has been in the business since fintech’s inception. We know how to build valuable web and mobile platforms that meet all fintech compliance regulations. Call us and get your smart solution underway, don’t give your rivals a chance to overtake you, let’s start working on your platform today.