Digital Banking Trends: Is the Post-Pandemic Storm a New Beginning?

Market Researcher

Several industries have been forever changed by Covid-19, and the financial sector is no exception. In 2019, most banks, from small local ones to multinationals such as JPMorgan Chase & Co., thought they were prepared for any scenario. In 2022, however, these financial institutions have been forced to reinvent themselves, otherwise, they risk disappearing.

There are two reasons for this. First, the pandemic-driven shift in customer behaviour and demand made digitisation more pressing. Second, fintechs turned out to be more serious rivals than they once seemed. At the start of the pandemic, fintech companies offered a superior online customer experience powered by advanced technologies and lower fees, which allowed them to poach clients from traditional banks.

Galileo’s 2021 State of Consumer Banking and Money poll showed that 62% of U.S. consumers were ready to switch to a digital-only bank, and this figure will continue to increase. To remain competitive, banks cannot provide less than fintechs. It's high time to focus on new business models, digital transformation and innovative trends.

An interesting trend phenomenon is the emergence of neobanks, also known as challenger banks — online-only financial institutions without traditional branch networks.

MadAppGang has developed digital transformation and fintech products for years. We've been watching digitalisation evolve since its early days and want to share our observations and experience with you. This article provides an overview of key digital banking trends and discusses the technologies that can help financial organisations become more innovative.

Key digital banking technology trends in 2022

Here are the major digital banking trends shaping the future vision of banking and contributing to competitive and innovative banking software:

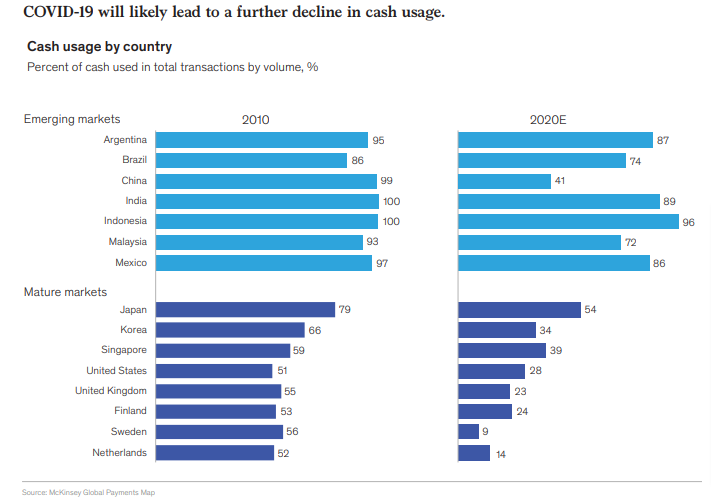

The growth of online transactions

While this trend in banking is not new, it accelerated significantly with Covid restrictions and the general shift to remote operations. But the trend isn’t entirely down to Covid alone. Other contributing factors include governments decreasing the amount of cash within the anti-money laundering policy. Using less paper, machines, and metal is encouraged by green initiatives and a lack of natural resources. And, let's not forget that people use eCommerce stores more often, paying for goods and services online.

When planning a digital transformation or upgrading your online or mobile banking service, take this trend seriously. It's crucial to remain a reliable service provider and to endure the harsh competition. For the same reason, it's wise to introduce some payment-related trends, too.

Understanding the differences between online and mobile banking is also important.

Innovation in payments

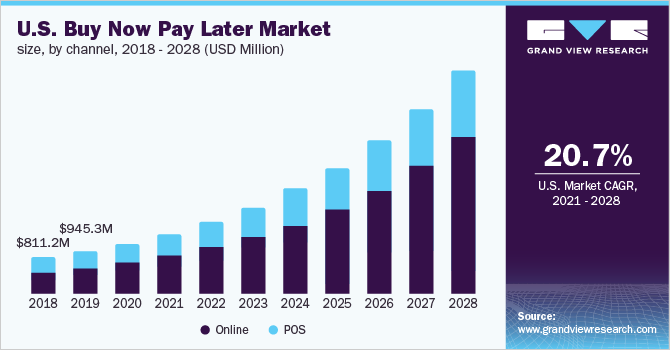

The real-time payments trend and demand for Buy Now Pay Later (BNPL) loans continue to expand. Within a few years, the BNPL lending industry in the U.S. has grown into a US$100 billion business. Little wonder as with BNPL, users have a very convenient interest-free credit option, and banks offering BNPL gain a competitive edge by capturing more market share.

A key banking technology trend, real-time payments provide greater visibility by improving cash management and enhancing businesses' day-to-day operations. Due to the unquestionable value that real-time payments provide, this sector is expected to record phenomenal gains of US$99 billion by 2028.

Simplified access to banking products

The top priority of modern customers is to spend as little time and effort as possible. In response, banks have been striving to simplify and streamline access to banking products and services for customers. Without forgetting about security, though. Technologies such as multi-factor and biometric authorisation make accessing digital bank services easy and safe.

This trend to digitalise existing services helps global financial inclusion, too. Online account management, instant support, and innovative tools are of significant help to people who do not have local access to banking services. Adaptive technologies, such as speech recognition systems and AI tools can be life-changing for people with disabilities.

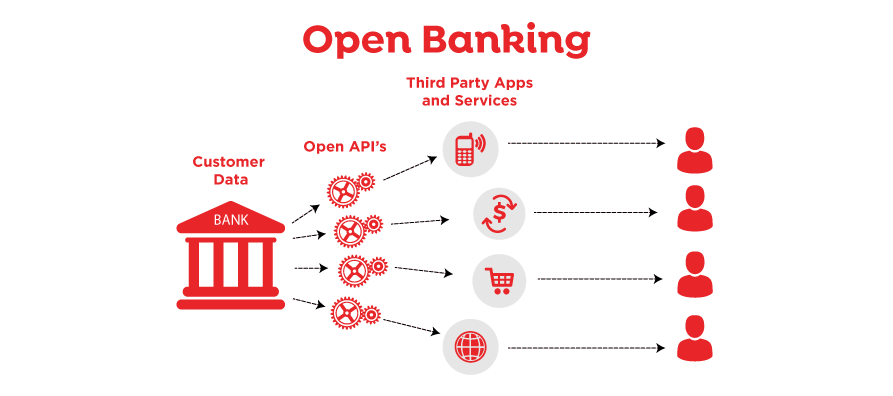

Open Banking

Open banking allows third-party applications to access consumer data and enables the networking of accounts and data across financial service providers. Banks can then provide increased value to customers via a connected ecosystem of financial services. For the customer, open banking makes it easier to apply for a new credit card, change banks, and use budgeting and investment apps within one account.

Source: Medium

For many, the concept of sharing customers' data with third parties still seems disturbing. However, it's just as safe as standard online banking as data is only shared with verified third parties and with the user's consent. Hence, we'll see some significant movement towards open banking even by the end of 2022.

Personalisation

The concept is not revolutionary but it’ll remain one of the main trends in banking for a while. A bank differentiates products according to customer profiles: profession, income level, credit history, and so on. By doing so, banks can provide relevant services to customers and increase their loyalty. Yet, the increased digitalisation of financial institutions and the competition from fintechs means a more advanced and innovative approach is needed.

Advanced personalisation typically involves AI and Machine Learning (ML) algorithms for in-depth data analysis, chatbots for immediate help, and, in some cases, personal advice by a qualified expert through live chat. When implementing all these technologies, don't overlook design personalisation. User-centric design — visualisations, gamification, and intuitive navigation — has become a crucial factor for many users when choosing a bank.

A hyper-personalisation framework representation. Source: Toolbox

Automation

Many banks are using automation to streamline banking processes as part of their digital transformation strategy. Besides helping banks reduce processing costs and boost branch productivity, automation helps with handling other challenging tasks. For instance, ML and AI algorithms can be used to detect abnormal account activity and prevent fraud.

The automation of marketing tasks, such as gathering and analysing customer feedback or sending push notifications, has proven invaluable in the day-to-day workflow. Banks that automate routine tasks are better equipped to focus on strategic matters, such as personalisation and customer care, which can include both regular support and financial advice.

Paperless documentation

Electronic documents are still more of a trend than a norm in 2022. Many banks, however, are working to completely eliminate paper. This includes not only making it possible for customers to open accounts, pay taxes, and complete other financial transactions online without leaving the app, but also optimising internal workflows. Here are a few reasons why:

- Remote work makes the use of paper documentation unmanageable

- Paperless business is a rewarding and eco-friendly practice

- Paperless documentation significantly reduces transaction time, improving the customer experience

- Major savings on paper, ink, envelopes, and so on

How the migration to cloud-native technologies aids digital transformation

To speed up digital transformation and follow current trends, big banks leverage cloud-native technologies. In 2020, Capital One became the first U.S. bank to shutter its on-site data centres and shift to an all-cloud IT environment. And it won’t be the last financial institution to do so. Capital One's experience showed that moving to the cloud is an efficient way to cope with post-Covid challenges and stay up to date with digital banking trends.

In her article, Allison Perkel, a tech leader from Capital One, focuses on how moving to the cloud helped Capital One cope with the Covid shutdowns. Due to its lack of on-site data centres, the company could prioritise its workforce's health while still maintaining control over its infrastructure and productivity.

However, it was not the only advantage. Key benefits of the cloud-native approach for Capital One and other financial institutions can be divided into three groups. Let’s take a closer look:

Reduced costs and improved competitiveness

By embracing cloud-native platforms, financial institutions can compete with fintechs more effectively. Firstly, companies can launch innovative products as quickly as competitors. Secondly, they can optimise business costs, and, consequently, offer cheaper loans and lower operational fees to clients. By using the services of big cloud vendors such as AWS or Google Cloud, millions can be saved on data centres, brick-and-mortar offices, and tech departments since cloud vendors handle the majority of routine tasks.

Increasing online operations

The cloud-native approach aims to build highly scalable systems by combining multiple technologies (distributed architecture, application programming interfaces (APIs), stateless applications, and the like). When the number of transactions increases, you can almost instantly create the necessary number of service copies and increase the capacity.

Distributed architecture allows for the microservices that can be scaled independently as needed and without affecting the system as a whole. Microservices are stateless, which means that previous transaction data isn't stored on the server. Because the service does not store any data, a load balancer can copy it endlessly and distribute requests amongst the copies.

As well, such a structure allows you to scale down resources when needed, thereby saving you money. Cloud vendors use pay-per-use models based on resource consumption. In other words, there is no need to overpay just because you expect traffic to grow.

Agility and innovation

Using the cloud-native approach makes institutions better able to adopt new innovations in several ways. First, the approach’s principles — standardisation, automation, and continuous delivery — help to speed up the development and implementation of innovations such as AI algorithms. Second, organisations can use pre-built cloud AI solutions and access data lakes via the cloud for their applications. And finally, cloud-native software based on microservices provides a strong foundation for open banking, allowing you to connect your platform with third-party apps via APIs.

Final word

The cloud-native approach is the most effective method for keeping up with digital banking trends and enabling digital transformation at financial institutions. By adopting cloud-native technologies, your business can reap the benefits of scalability, agility, quick innovation adoption, cost-efficiency, and more.

It is vital, however, to understand that creating cloud-first solutions is not all roses. It's not just a different approach to designing and architecting applications, but also to organising business processes. Adapting a company to cloud-native represents a major change to its DNA. To take full advantage of cloud computing, companies must undergo a digital transformation that goes far beyond a simple project. And it requires lots of zest and work.

Even if you have an in-house IT team, you will need the help of experienced professionals like MadAppGang. If you trust your project to us, not only will our experts help you develop complex solutions and services, but they will also help you organise the processes in line with cloud-native culture. Let's talk in detail about your project and start transforming your financial institution.