What Is a Neobank? A Starter Guide for Entrepreneurs

Market Researcher

Thinking about launching a startup? If so, you might have considered building a fintech application, such as a neobank.

A rapidly growing sector, the global neobanking market was valued at US$47 billion in 2021 and is expected to reach over US$2 billion by 2030. With the right marketing strategy and a clever software solution, you might be able to get a significant share of the digital banking pie.

At MadAppGang, we have an extensive track record building fintech solutions, from the dawn of fintech with Webmoney in the 00s to innovative financial projects like Getswif. Based on our experience, we created this 101 guide to neobanks to show you how this business works and the challenges you might face. To start, let's clarify what neobanks are.

What is a neobank?

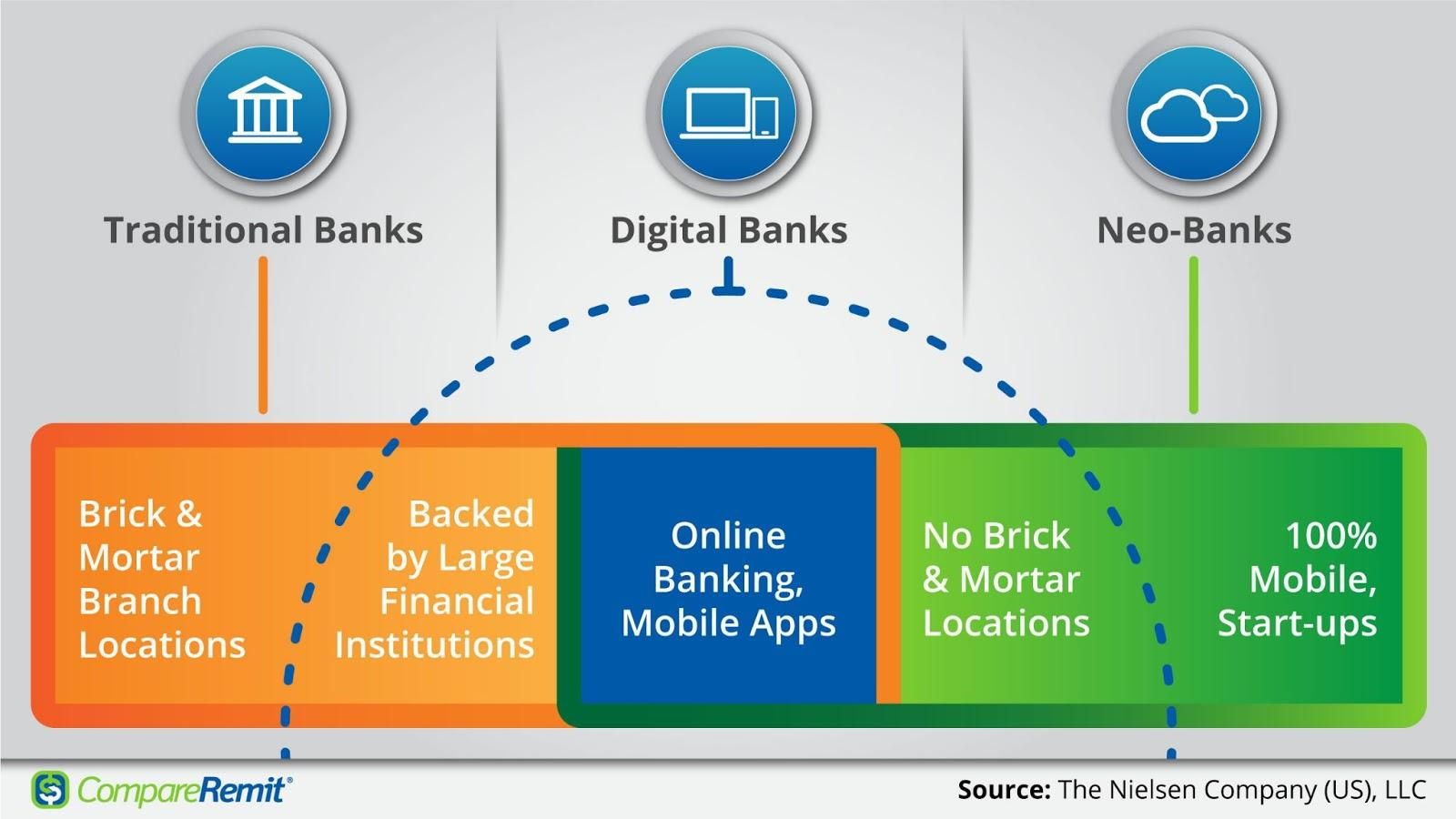

Neobanks, also known as challenger banks, are online-only financial institutions without traditional branch networks. They are essentially fintech companies that use advanced technologies to streamline banking and provide an online alternative to brick-and-mortar banking. The features and structure of neobanks aren't identical, but they typically differ from credit unions and traditional banks (online banking services included) in the following ways:

- State or federal regulators don't regulate neobanks in the same way as banks

- Neobanks are primarily designed for mobile devices

- To insure customer deposits, neobanks partner with traditional banks

- For risk and cost reduction, neobanks offer limited or no credit

In recent years, however, a number of neobanks have obtained banking licences, including Monzo, N26, and Starling Bank. Today, we can classify neobanks into the following groups:

Neobanks with a banking licence – Some of the popular neobanks are licensed banks, either specialised or full-range. These ‘challenger banks’ offer the majority of banking services: checking and savings accounts, debit and credit cards, loans, currency exchange, money transfers, and peer-to-peer payments. Examples: Atom Bank, N26, Monzo, Revolut, and Starling Bank.

Neobanks without a banking licence – These companies provide financial services under the licence of other banks. They can either create their own financial products or just provide additional banking tools to certain banks' customers. Examples: Chime Bank, Simple, Revolut, Yolt.

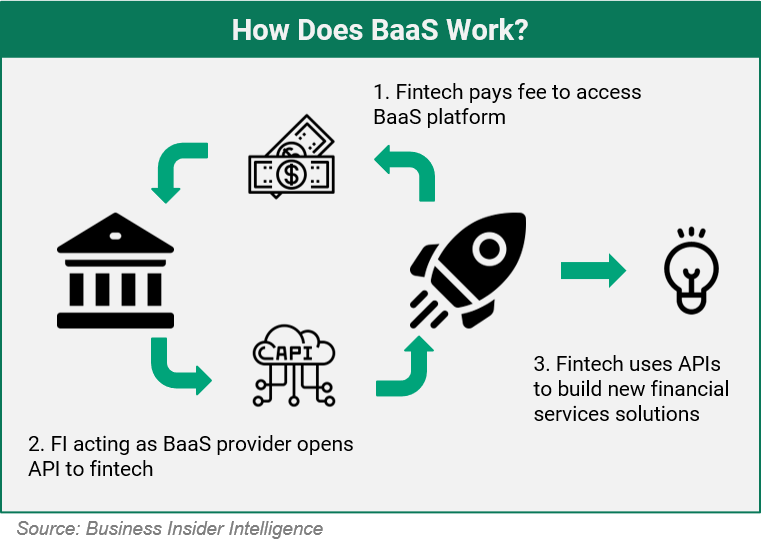

Banking as a Service (BaaS) – A BaaS is a white-label banking platform that allows businesses to incorporate financial services into their products and allows banks to add technological innovations to their services. Simply put, BaaS platforms consist of 3 layers: traditional, licensed banks, a range of fintech services, and the application programming interfaces (APIs) that connect these layers. With BaaS, banks can provide multiple APIs, which other firms or individuals may use to develop their own solutions. These solutions help banks to promote themselves, provide better customer service, and reduce total human effort.

How do neobanks make money?

When building a neobank, an entrepreneur should not only focus on the features and innovations their product can offer, but also find a way to make their business profitable.

Neobank vs traditional bank strategies

Due to differences in regulations, licensing, and such, a neobank cannot simply copy the strategies of a traditional bank, nor is it feasible. The alternative is to use some conventional models or adopt newer, hybrid strategies to achieve profitability. Today, the most common business models for neobanks are:

Interchange-led

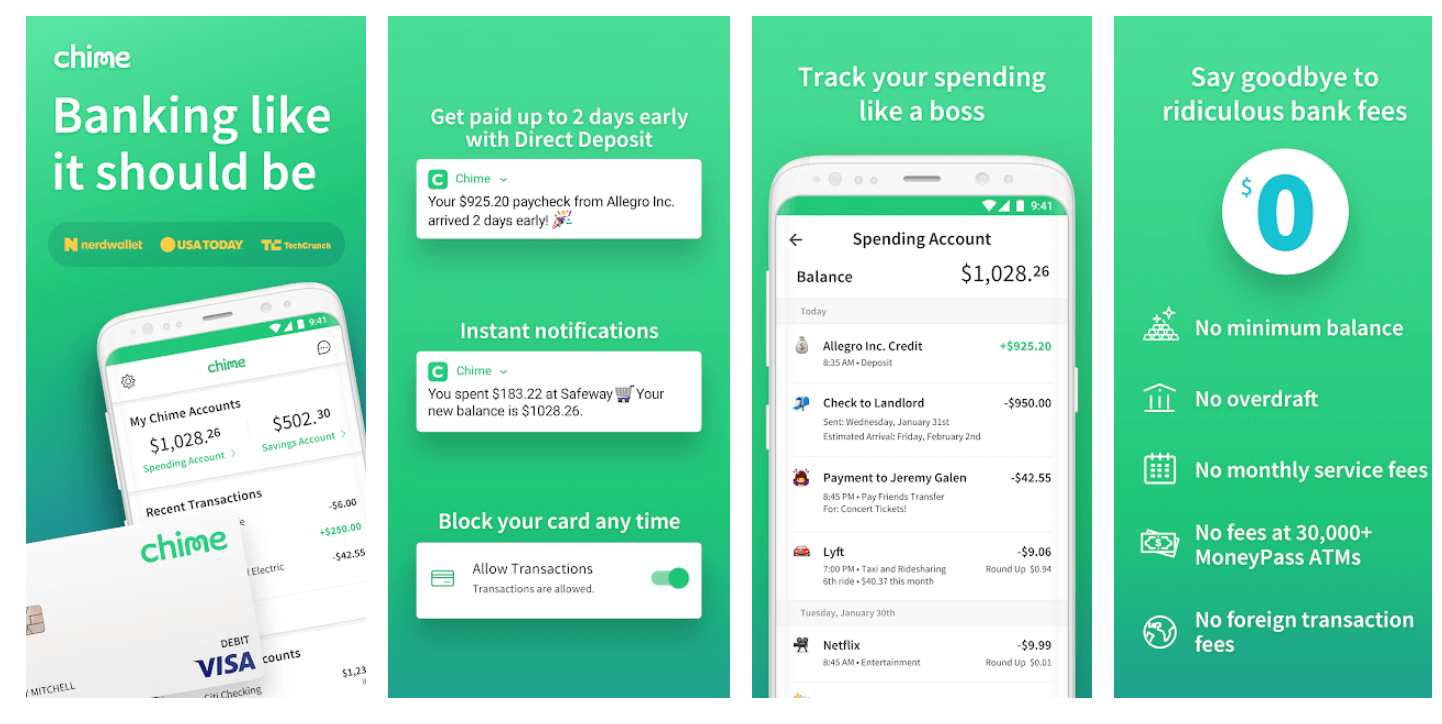

Several neobanks around the world use this model, including Chime in the U.S. and Neon in Brazil. Chime, for example, receives a portion of the Visa transaction fees when a customer uses their Chime Visa card. The company also earns interest on ATM fees and cash transactions. For Chime, this strategy has proven beneficial: from one million accounts in 2018 to 12 million in 2021, this neobank's clientele grew twelvefold.

The Chime app. Source: Chime

Credit-led

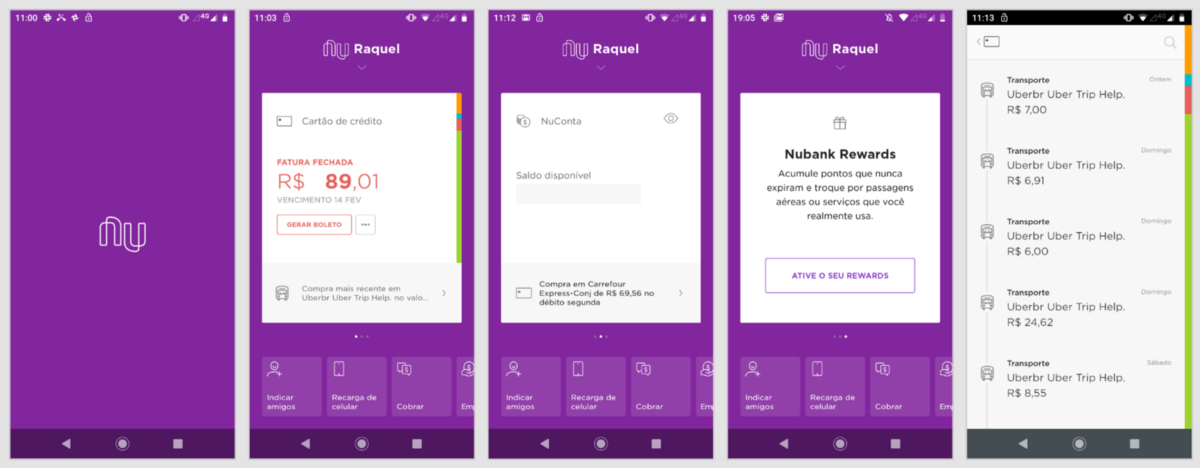

This model allows neobanks to profit by applying interest rates to customers’ credit-card balances. They provide credit-first services, such as the issuing of credit cards, and later offer debit bank accounts and other services. Furthermore, some neobanks (NuBank in Brazil, Freo in India, and Finclusion in several African countries) combine their credit-led model with an intercharge strategy to improve profit margins.

The NuBank app. Source: Medium

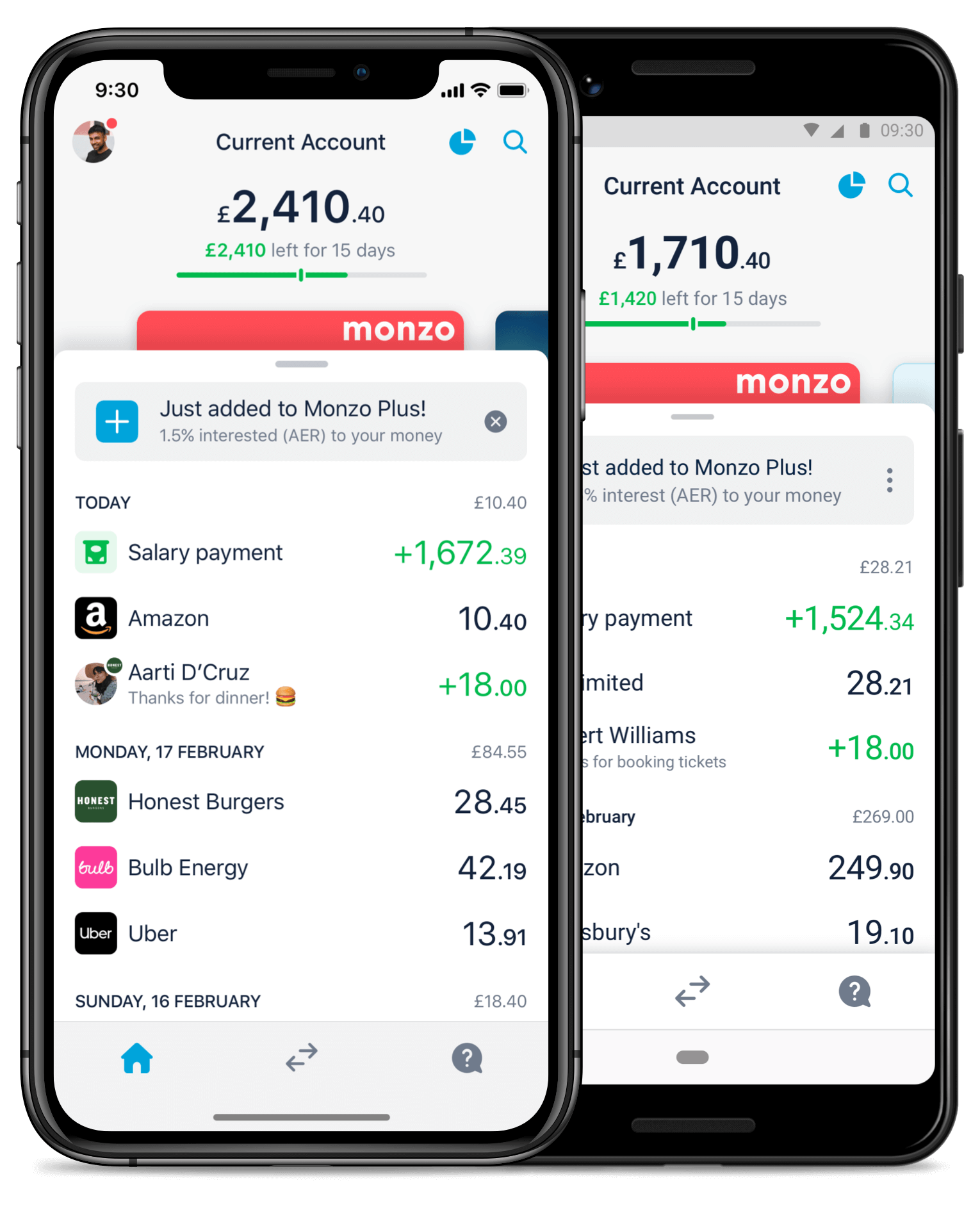

Ecosystem-led

In this model, a neobank functions as a marketplace for financial products and services, such as investments, cryptocurrency trades, insurance, loans, and so forth. A good example here is Monzo, a major UK neobank. Partnering with PayPoint, it enabled its customers to deposit cash from any PayPoint location across the UK. Savings accounts are offered to Monzo customers through partnerships with banks and asset management companies (ParagonSave, Shawbrook). Also, through its partnership with Wise, Monzo provides international money transfers in its app.

The Monzo app. Source: Monzo

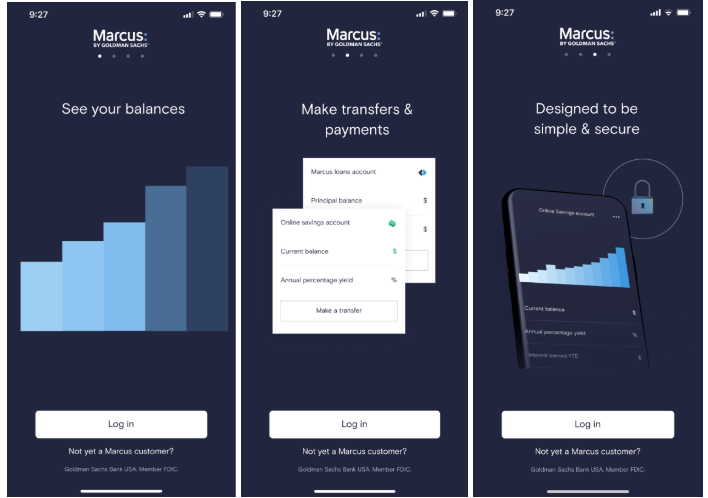

Asset-led

This business model assumes that fintech banks earn on deposits. Unlike other neobanks, these financial institutions do not offer a wide range of services to consumers, but they do offer checking and high-yield savings accounts, cash advances, high-yield certificates of deposit (CDs), and no-fee personal loans. A good example here is Marcus, which had US$97 billion in deposits by the end of 2020 and plans to have at least US$125 billion by 2024, despite lacking physical branches.

The Marcus app. Source: Marcus

Product extensions

When talking about neobanks, a product extension may refer to any fintech app (be it for budgeting, investment, cryptotrade, or insurance) that can be connected to a traditional or neobank account. Normally, such apps bring additional value to the main service bundle. For example, Robinhood Gold, an extension to the Robinhood app, offers access to deposits, professional research, Nasdaq Level II market data, and margin investing for a monthly fee of US$5 to $50.

The Robinhood app. Source: Money

Neobank challenges

Neobanks are currently trendy fintech apps as they upgrade existing banking experiences, plus offer an easier and faster way to manage personal finances. However, neobanks do face some challenges. Let’s name a few:

Profitability – Despite their popularity, a number of prominent neobanks still struggle for stable profit growth. For instance, UK-based Revolut's 2020 revenue grew by 34% to US$310.5 million. In the same period, however, its losses increased by 57% to $217 million.

Compliance – The regulatory system raises barriers for everyone. For instance, in Europe, fintech compliance practices vary from country to country and fall under multiple jurisdictions. It's also worth noting that the requirements are growing tougher, especially after N26's weak Anti-Money Laundering (AML) fines as well as Monzo's current money-laundering investigation.

Security – Neobanks store sensitive information such as identity data, passwords, bank account data, and so forth. Third-party components (payment gateways, analytics systems, chatbots, and so on) can potentially compromise the security of any product. At a minimum, financial institutions must comply with general (PCI DSS) and local regulations to prevent security issues.

Manual processes and inefficiencies – Doubled customer records, the siloed data from legacy systems, add further complexity and increase risk, costs, and implementation time for new systems.

Customers value differentiation – Neobanks need a large customer base in order to make money, and that means encouraging people to switch from traditional banks and competing fintechs. As a result, it is crucial to follow mobile banking trends and differentiate any product with a unique package of services and features: favourable loans, AI-powered tools, and so on.

Neo digital bank: Is the venture worth the effort?

The list above seems to represent a huge pile of problems. However, there is a solution to all of them. In terms of monetisation and profitability, finding the right niche and building a strong marketing and profitability strategy is the most viable solution. Studying the market, your competition, and identifying service gaps is an effective ways to start. Providing unique services or tools may become the differentiator that helps your venture succeed.

To provide these unique services and ensure any banking software is both secure and stable, all sorts of fintechs adopt a cloud-native approach. A modern Agile workflow combined with cloud-based tools and the cloud’s potential help address most of the problems in discussion. Big cloud providers can cater to almost any challenge you may face with a fintech or neobank project. Using Neo4j Aura on Google Cloud, for example, helps to automate the process and reduce manual work and errors. Machine Learning tools from AWS help prevent online fraud. AI tools provided by Azure help deliver tailored user experiences.

Although moving to the cloud and building a cloud-native platform may seem like an uphill task, it's easier if you have the right people on board. A team like MadAppGang brings years of experience and reliability to the table, so you can be sure of a high-quality final product. The banking products we build are secure, user-friendly, and packed with advanced features and tools. If that's what you are looking for, contact us and let's discuss your project in detail.