Fintech’s Impact on Banks: Revolution for the Sake of Evolution

Market Researcher

Will fintech kill banking? Probably not. But there’s no doubt that fintech is changing banking. Through technologies such as artificial intelligence (AI), machine learning (ML), the Internet of Things (IoT) and blockchain, fintechs have changed the face of the finance industry and redefined customer preferences and expectations.

MadAppGang has worked in fintech since its early days and has seen the industry evolve. Here, we examine fintech’s impact on the banking industry and look at how financial institutions are approaching the digital revolution. But first, let's clarify the notion of "fintech" and its origins.

The rise of fintech

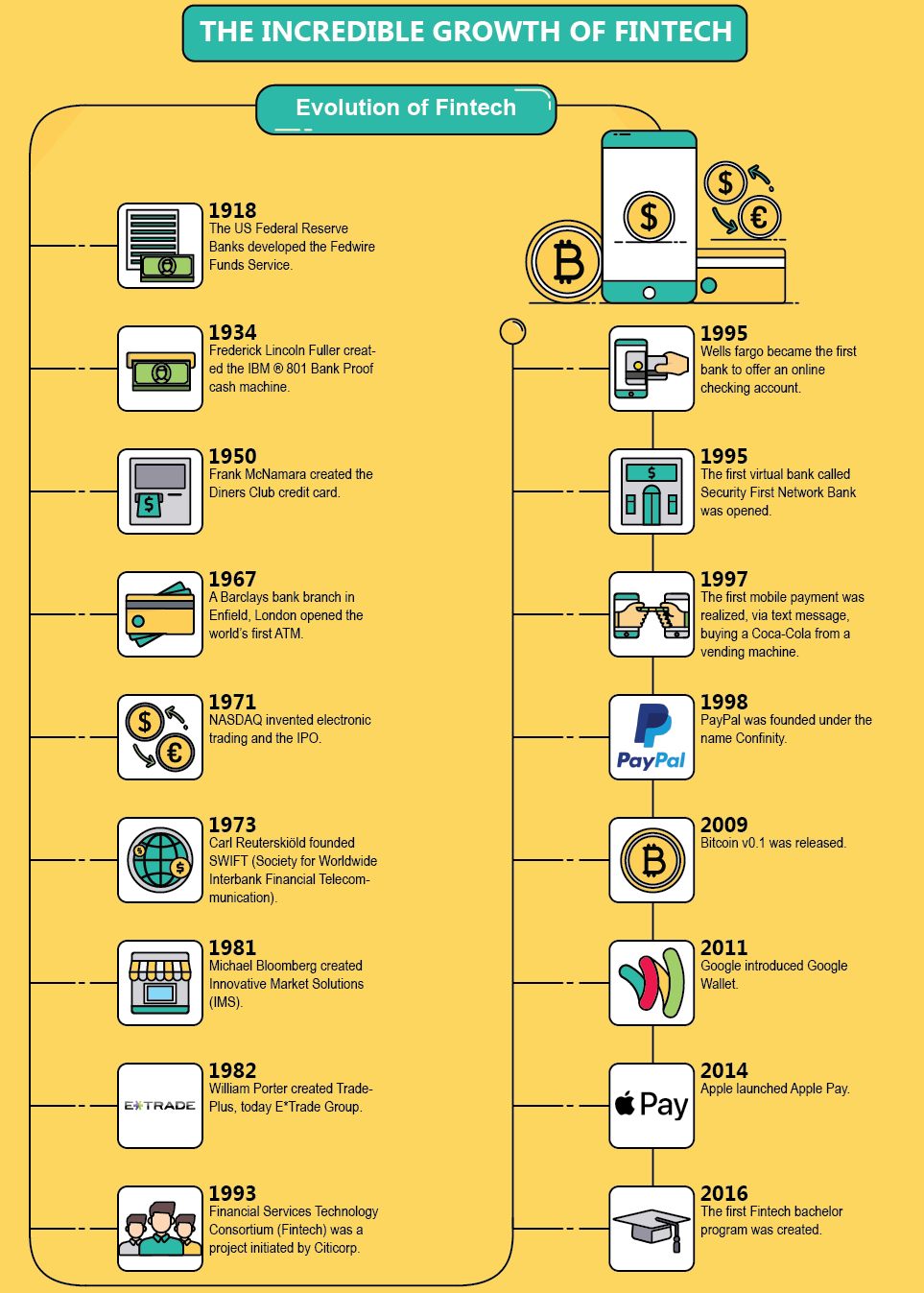

Fintech, is financial technology, that is, the use of technology to improve financial services. The term may have been coined in the 21st century, but financial technology has shaped how we interact with our money for over 100 years. Historically, fintech dates back to the late 19th century. Back then, money could be transferred via telegrams and morse code — but it's unlikely investors would be thrilled about this in today's world.

Fintech today is a booming industry driven by far more advanced technologies than telegraphs or landlines. Instead we have smartphones, advanced software, and lightning-fast internet connections. Fintech is only expected to grow in the next five years. By 2026, the market is expected to be worth US$324 billion. Yet fintech is still often misinterpreted as a copy-paste of existing financial processes and institutions into the digital world.

Source: Holytransaction

However, that's not the case. Fintech is traditional banking's rival and catalyst for change. The 2008 financial crisis provoked a widespread lack of trust in established financial institutions and made people turn to new financial practices. Customers were drawn by more accessible and faster services and lower fees offered by digital startups. For example, in Russia, the online payment system WebMoney offer fast, safe, and convenient online payments and transfers with easy sign-ups and attractive exchange rates.

And it doesn't matter how much of the banking market share fintechs gain or lose, they continue to develop new business models and redefine the customer expectations. To stay competitive as fintech companies alter the face of finance, banks must adopt new practices.

How fintech is changing banking

Fintech’s impact on banking is already visible. Since Zopa, a UK peer to peer lending platform was launched in 2005, and we first heard the word fintech, things changed drastically. In 2021 we don't have to go to a branch to transfer money abroad, make a mortgage request, or check our credit score. It's all possible due to fintech's disruptive business models.

Source: Pinterest

How does fintech affect banks? In general, fintech changes the global financial industry in two main ways:

Going customer-centric – Unlike traditional banking, fintech puts the customers in the spotlight. Offering just one or two types of product or service, financial technology companies concentrate on doing the job well and going above and beyond customer expectations.

Going fully digital – Digital solutions, such as mobile banking apps, allow customers to open accounts, pay bills, and conduct other transactions remotely. It’s time-saving and convenient, especially in the context of Covid-19 lockdowns.

Ditching traditional banking practices, financial technology companies optimised staffing and reduced costs. This translated into lowered service fees for the customers, making fintech products even more advantageous for users.

Lower fees and real-time remote payments caused a rapid shift in how consumers view financial services companies. To remain competitive, banks accelerated their adoption of new practices and technologies. As evidence of this, financial institutions have invested more than US$27 billion in digital innovations since 2015.

Leveraging technologies helped banks such as CenterState Bank build better banking architectures, increase processing speeds and optimise staffing and workflow. In turn, this lowered transaction fees, reduced loan costs, and allowed clients to obtain products tailored to their needs. Overall, it bettered the banking experience for customers and allowed banks to compete with fintechs, for now at least.

Fintech shaping the future of banking

How will fintech change banking in future? Financial institutions will continue monitoring fintech’s advances. Some are taking a defensive approach, looking to retain what they already have and not branch out further. Others are seeking growth and building advanced fintech solutions in-house. As yet, neither strategy has proven “correct”, but integration aka “fintegration” is the mainstream approach.

The “Fintegration” trend

Fintegration is the collaboration of banks and fintech companies. On the one hand, this collaboration enables banks to tap into agility, innovation, and the technological strength of fintech firms. On the other hand, it allows fintechs to make good use of banks' reputations, experience, and capital.

The 2015 Disruption of Banking report by the Economist names fintegration as a highly plausible scenario. The relative strengths and weaknesses of banks and fintech firms are more complementary than competitive, meaning a fintech-banking industry collaboration is a win-win situation. The benefits of fintegration include:

For banks:

- Improved customer experience

- Access to cutting-edge services including artificial intelligence, blockchain, and key mobile banking trends such as open banking solutions

- Enhanced processing efficiency

- Reduced costs

For fintechs:

- Possibility to scale business and improve ROI

- Better funding

- Improved risk management

- Wider customer reach

For customers:

- Wider range of innovative financial products

- Faster transactions and responses to requests for products such as loans or mortgages

- Higher level of cybersecurity powered by advanced technologies such as blockchain

- Deposit security guaranteed by regulatory authorities

- Lower service fees

Fintech banking solutions

For some time now, banks and fintechs have worked together and developed partnerships. Some of these collaborations have resulted in innovative solutions. Here are some examples of fintech solutions being put to use by major banks:

ABN Amro and Tink

Dutch bank ABN Amro partnered with Swedish fintech Tink to create a solution to engage consumers and retain its market share. The result is Grip, a personal finance app that allows users to manage accounts in six different Dutch banks simultaneously. With over 500,000 downloads, Grip is among the top finance apps in the Netherlands.

Source: ABN Amro

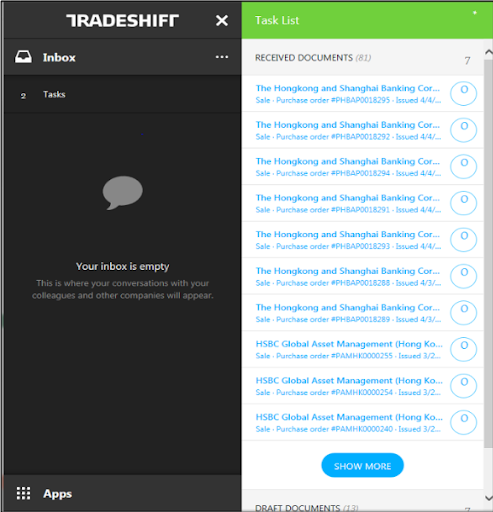

HSBC and Tradeshift

In 2017, HSBC announced its partnership with Tradeshift, a global supply chain finance company. Under this agreement, HSBC and Tradeshifts are developing a platform to automate supply chain processes, and expedite and add transparency to lengthy payment cycles.

Source: HSBC

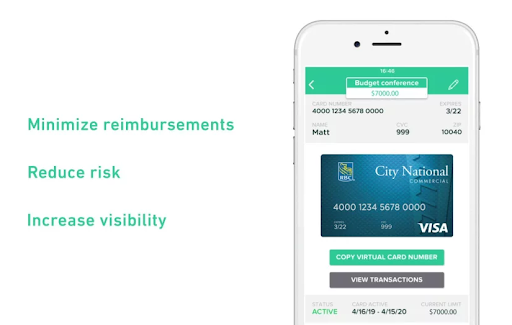

City National Bank and Extend

City National Bank partnered with fintech startup Extend to launch a virtual Visa credit card solution. The new solution enables clients to issue virtual credit cards connected to Apple Pay and Google Pay mobile wallets for easy and contactless payments. Visa Virtual enhances e-commerce capabilities, allows companies to set spending limits and expiration dates, and get greater control over corporate cards.

Source: CNB

The final word

As you can see, there's a promising future for banks and fintech companies working together. Together, financial technology and banking can bring innovative financial solutions to the market quickly and cost-effectively. This is a favourable situation for all stakeholders, and also for the customer, who gets advanced financial products and services at a lower price.

Now is an excellent time to launch your fintech company and find a bank to partner with. And, it may happen that your fintech will change banking even further. "The first step is to establish that something is possible then probability will occur."― Elon Musk.

Let's discuss your idea. The technical work is on us, just share your vision with MadAppGang. Our team will use all of its experience and knowledge to deliver a ready-to-market fintech solution for iOS, Android, and or the web, in full accordance with fintech compliance regulations.