A Concise Guide to Building a Fintech App

Market Researcher

Financial technology (fintech) solutions make financial operations safer and more convenient for banking institutions and consumers alike. Fintechs have transformed the way we approach general banking, account management, investments, and more.

The number of mobile banking startups is increasing year on year, with the pandemic stimulating this growth further. Early 2020 data showed a steady surge in fintech app engagement: banking, payment, and investment apps experienced increases of 26%, 49%, and 88% respectively to the number of sessions. The boost to fintech startup investments is even more impressive: venture capital firms ploughed slightly over US$1 billion into new products in 2019 and over US$91.5 billion in 2021.

Even though there are thousands of fintechs competing for customers and investors, demand isn’t shrinking. No surprise as fintech covers numerous areas and there are plenty of challenges left to solve in the still burgeoning industry.

To get in on the action, you need to know how to build a fintech app. Here, we cover some of the basics including fintech app types and categories, the trends shaping the industry’s future, and the must-have features in fintech products.

Fintech business models

Fintech apps can be divided into several types and categories:

Payments and money transfers

Consumers increasingly choose digital payments over cash. They need easy-to-use solutions for different financial operations, from online purchases and international transfers to peer-to-peer lending. Online and mobile payment apps cover these needs the best.

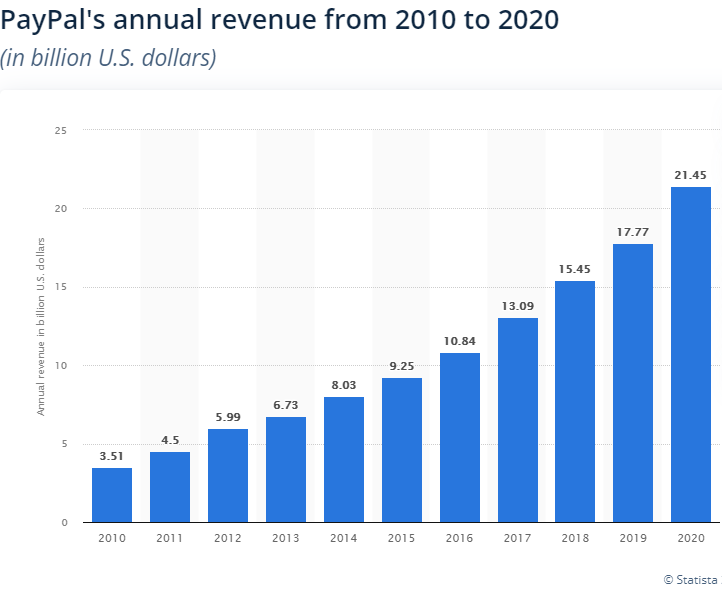

One of the best-known online payment systems is PayPal, a fintech platform that eases money transfers, and lets you pay with a bank account instead of a credit card online, while keeping your payment information private.

PayPal enables easy, fast and cheap transactions worldwide. No wonder its popularity (and consequently its revenue) grows every year. In the past decade, PayPal's revenue grew sevenfold to US$21.45 billion in 2020.

However, even giants such as PayPal face challenges. Rivalry in the sector is growing as more players (Venmo, Skrill, Payoneer) appear.

Digital banking

Most banks offer mobile apps as a convenient alternative to visiting a physical branch, but digital-only or neobanks such as Monzo, N26, and Nubank have ditched branches entirely and are competing with traditional institutions.

Today, Chime is the most valuable American neobank. Since December 2019, its value has more than doubled and is now worth almost 900% more than it was 18 months ago, when it hit a US$1.5 billion dollar valuation. CNBC ranked Chime 25th on its 2020 Disruptor 50 list.

Chime app user interface. Source: Chime

Today, Chime is on the rise. However, like its counterparts, it also faces challenges. One of these challenges is to reach profitability as most customers don’t use neobanks as their primary account. Accordingly, digital banking’s focus is now on gaining more customer trust.

For entrepreneurs launching a neobank, there's a strong need to meet fintech compliance regulations while simultaneously focusing on building long-term relationships with customers. Excellent 24/7support and advanced security to prevent privacy and data leaks build trust.

Personal finances and savings

Wealth management, credit monitoring, and personal finance analytics are in high demand among consumers who want control over their finances with minimum effort. The leader in this category is Mint, which enables users to track spending, create budgets, and get daily, weekly or monthly financial overviews.

The Mint app.

There's always room for improvement, though, and that's why Mint’s rivals strive for improved functionality and design. For example, Copilot, a new personal finance-tracking app, offers both slick design and advanced money management features, such as the ability to create custom categories for transactions.

The Copilot app.

As a variation of personal finance managers, there are corporate banking fintechs and business finance apps. These services help manage employee expenses, payrolls, and taxes, as well as automate bookkeeping processes. Some examples include Expensify and Zoho Expense.

Subscription payment management in the Truebill app. Source: Truebill

Insurance

By 2027, the global InsureTech market is expected to be worth US$11.94 billion. InsureTech is growing steadily, so it's no surprise that it produces promising startups. For instance, there’s Teambrella, a peer-to-peer insurance platform powered by blockchain. With Teambrella, one can join or create a team and a collective wallet for emergency use.

The Teambrella app. Source: Apkpure

If you plan to build a classic InsureTech app, there are a plethora of examples to reference: Lemonade, Cover Esurance and others. Your product will have to compete with these apps and face the same challenges such as integration with legacy systems and the changing economic landscape.

Cryptocurrency purchases and trading

With crypto markets firmly established in the financial world, fintechs have emerged to help users buy and sell digital currencies and receive trading insights. This industry is highly competitive, so creating a smart and secure cryptocurrency app is essential. BitPay and CoinBase are good illustrations of cryptocurrency fintech apps.

The Coinbase app interface.

The main concern with cryptocurrency platforms is security. At the earliest stages of planning and building a cryptocurrency app, you have to consider how you’ll create a highly secure end-product.

Investments

Mobile fintech has made buying and trading stocks and securities more accessible and straightforward. Robo-advisors — online services that automate investments and help users build strong investment portfolios based on algorithm-driven insights — are increasingly popular in this niche.

Most people are used to thinking that investment platforms offer just stocks and cryptocurrency buying. Meanwhile, investment apps offer a variety of choices. Here are a few examples:

- Primary investments in private companies: AngelList, iAngels, FundersClub, Manhattan Street Capital, MicroVentures, Nasdaq Private Markets.

- Secondary stakes in tech companies: CartaX, Equityzen, Sharespost/Forge.

- Investments in real estate: PeerRealty, RealCrowd, RealtyMogul, AcreTrader.

- Cryptocurrency trade: Binance, Coinbase, eToro, Gemini.

- Investments in art and collectibles: Vinovest, Otis, Rally, Yieldstreet.

Having said that, there are plenty of potential investment app niches worth exploring. As with any fintech product, the rivalry among investment platforms is fierce. You’ll face the market’s challenges too, such as attracting investors.

Investment portfolio recommendations in the Wealthsimple app. Source: Wealthsimple

Crowdfunding platforms

These platforms allow anyone to raise funds for an early-stage project or social cause and integrate membership-based payments. A great alternative to traditional loans or peer-to-peer lending, crowdfunding is more popular than ever; the crowdfunding market is expected to reach US$24 billion by 2027.

Kickstarter and Patreon may be the first crowdfunding that come to mind, but plenty of niche platforms such as Gumroad, Ioby, and Crowdcube are also in demand. Despite rapid growth, there are numerous market sectors yet to be covered. You only need an original idea and a smart platform with high levels of security to build your crowdfunding unicorn.

Regtech

Regulation and compliance technology (regtech) is a range of services dedicated to solving compliance issues. It's a young and rapidly-growing fintech sector that is expected to be worth US$15.8 billion by 2026. Numerous regtech startups have sprung up to support financial institutions with compliance in an ever-changing regulatory environment.

Companies as 6clicks, Yoti, Paragon Data Labs, Apiax are designed to help organisations adapt to various fintech regulations. However, this doesn't mean that regtech companies don't have any challenges of their own. When creating a regtech startup, know that you'll need to guarantee bank-level data privacy as well as advanced security levels.

The regtech app 6clicks automates risk assessments and reviews. Source: App Store

So which choice will make your project successful?

The variety of solutions is truly diverse: new financial software companies are joining the competition by cooperating with existing institutions and creating new services. There are plenty of standalone applications with a particular functionality in addition to innovative platforms with application programming interfaces (APIs) and modular components others can use.

Regardless of the type of fintech project, to survive and succeed in this market, you need to define your application’s specific goals, learn your demographic and the features the user base demands, and understand the existing solutions in your niche. After it’s all done and you know what you want to develop, you’ll need a team of seasoned developers to discuss your project’s architecture, required integrations, and the scope of work overall.

At MadAppGang, we’ve been building solutions in the financial industry for over a decade and know how to develop a fintech app with top-class security measures and seamless UX. Check out the scope of our fintech software development services to learn more about our expertise.

Why enter the game?

Fintech solutions are gaining momentum because they make routine, and often stressful activities, easier and more transparent. Younger generations are the major driving force behind software innovations, so fintechs are increasingly adopting social network style features to make financial operations more user-friendly and more fun.

Fintech apps represent an opportunity to change the face of payments and money management for the better.

Financial inclusion

Millions of people worldwide are unbanked or underbanked. Their access is limited for a number of reasons, such as location, high bank fees, and such. Neobanks and payment systems contribute to financial inclusion by reducing fees, providing smart financial products, and ensuring greater security. Additionally, digital-only services are accessible from anywhere with an internet connection.

Boosting financial literacy

Even though it seems counterintuitive, the more digitised and accessible information is, the lower the level of financial literacy. For instance, 2020 data revealed that four out of seven Americans were unable to manage their finances. Fintech solutions targeted at consumer finance can help users better understand some financial concepts and feel more confident about their spendings and savings.

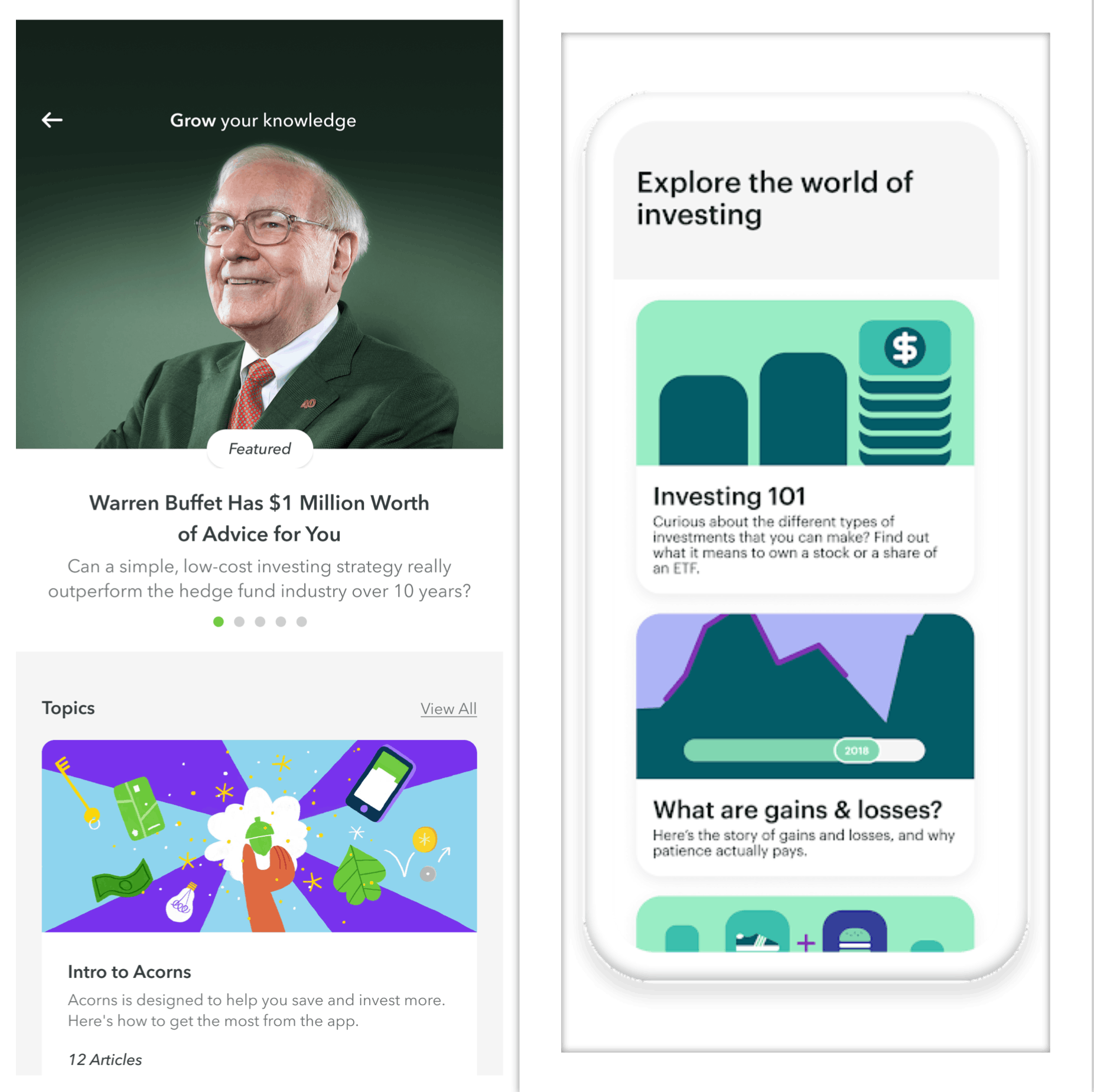

Given that some solutions are specifically designed to help consumers make better choices and understand their money, it’s not wishful thinking but reality. The key here is to provide users with simple yet informative messages and guide them through accessible financial operations and their nuances.

Educational sections in money apps Acorns and Greenlight. Source: Acorns, Greenlight

Making money operations more fun

Financial operations are often thought of as a chore and a bore, so solutions that add an element of fun and interactivity make a real splash. For instance, Venmo’s social media-like quality drives enormous engagement levels among Millennials and Gen Z, and as a result, it’s one of the fastest-growing payment apps. A big selling point for Venmo is that it makes payments fun with posts and comments, as well as emojis.

The Venmo app. Source: PCMag

Automating routine operations

Automation is the first benefit that comes to mind in the context of any consumer app. The way we handle our finances has changed dramatically over the years, becoming easier and faster thanks to automation. Small businesses get help with repetitive tasks like managing payments or retrieving reports. Individual customers (and entities too) can pay bills, send money, or buy stocks in a matter of a few taps.

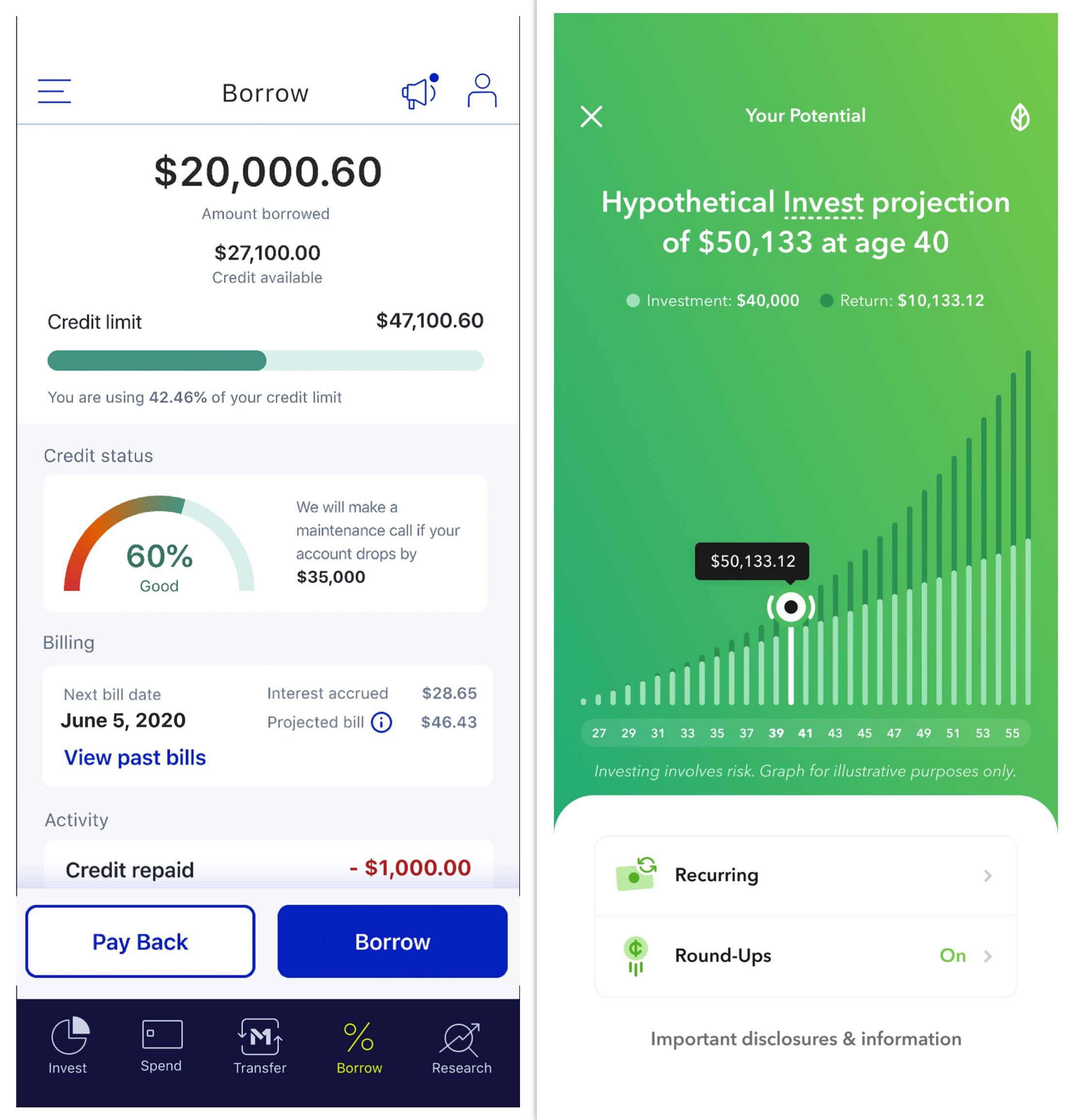

Users aren’t overburdened and they feel in control when every action is synced across digital tools and included in automatically generated analytical graphs. Automation solutions in fintech are experiencing a surge in investments, so you’re likely to strike gold when efficiently automating processes in a highly regulated area.

Automatically generated credit statistics in the M1 app and investment projection in the Acorns app. Sources: M1 Finance, Acorns.

Setting a technological trend

The leading technologies at use in fintech aren’t limited to automation. Industry leaders and new startups are experimenting with machine learning, computer vision, virtual assistance, voice recognition, and other innovations. The adoption of these technologies in fintech warrants a separate discussion, but in a nutshell, it’s worth expanding the market with an AI-powered solution.

Unifying financial processes

Thanks to global open banking initiatives, financial data can be used across multiple authorised solutions. The fintech space is growing, in part because of these initiatives; according to Juniper Research, the number of open banking users will exceed four billion by 2026. In the same year, the global open banking market is expected to reach US$43.15 billion.

Europe is leading the sector with government-supported programs for incorporating open banking frameworks and hundreds of authorised providers with access to open financial data. Even though it’s not yet widespread in the US, major American providers do have open banking strategies and a lot of apps targeted at American consumers collect data from open APIs.

Open banking standards and APIs lead to the unification of financial information, which, in turn, allows for easier connectivity between different solutions and an overall more efficient fintech infrastructure.

What to consider when building a fintech app

As with any other app, you’ll shape your idea in cooperation with developers who have relevant expertise, do research on the niche and target users, then design, build, and test the end product. But with fintech, you also need to take some extra steps, let’s discover which ones and why.

Straighten out regulatory frameworks

When you know what type of solution you’re going to build, and all the parties involved — consumers, banks, insurers, payment gateways — it’s time to figure out which regulations apply. You need to clearly understand all legal requirements associated with the financial data your app will use. Besides data specifics, fintech regulations depend on the country, so you also have to learn about the relevant laws in each of the locations you’re targeting.

Think security measures through

When dealing with sensitive data, any error comes at a tremendous price. In a fintech app, you have to ensure information security with the latest authentication technologies, up-to-date encryption, and any other measures relevant to the product. The test-driven approach to development (TDD), which usually makes the process longer and more expensive, makes sense in the context of fintech. With TDD, tests are written prior to development iterations, which reduces the number of defects and allows for greater security.

Figure out a way to be profitable

The main struggle for fintech apps, especially for neobanks, is reaching profitability. Even for digital banks valued at billions of dollars, such as Revolut, Chime, and N26, it takes years to become profitable. When developing your fintech product and building a marketing strategy, you need to find a way to beat the competition and reach profitability.

You may want to consider providing non-financial services to third parties and taking a commission on the leads. Alternatively, you could offer Banking-as-a-Service (BaaS) software that ensures the safe communication of data between banks and businesses. These businesses can then provide online banking services to customers without focusing on bank licences and integrations.

Focus on long-term relationships with the customers

Building customer trust is a major challenge for fintechs. As an example, only 10% of British consumers trust digital-only finance products. Most people have concerns about data privacy protection. Some fear the new ways of handling their finances. Others argue that technology is advancing faster than they can keep up with it.

Build long-term relationships with customers based on the highest level of data protection. Also, if you're planning a multinational brand, don't forget about proper localisation of your brand and product. Not only do you have to speak the same language as your customers, but also adapt to local user mentalities and purchasing and payment behaviours.

Design positive messaging

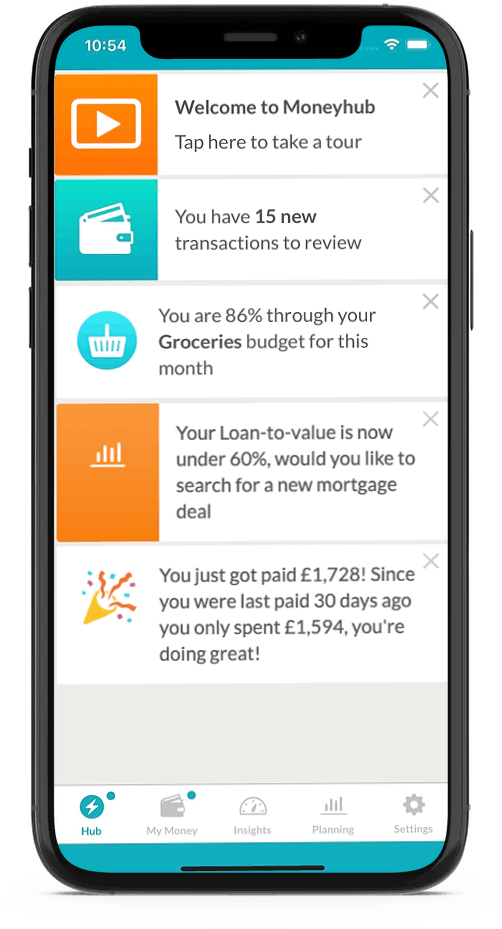

Fintech is an area that impacts and is directly connected to people’s well-being, so it’s crucial to maintain clear and positive messaging. Industry experts claim that driving positive behaviour is crucial to their success: Acorns’ CEO places a high value on badges and notifications that motivate users to “make good choices” and Moneyhub’s marketing head says that a fintech app should have a message that “everyone can understand and share.”

Notifications in the Moneyhub app. Source: Moneyhub

Consider partnering with banks

There is a trend for fintegration, a collaboration between banks and fintech companies. If your fintech company partners with a bank, it’s a win-win scenario. The bank will be able to offer new services and improve customer support. Meanwhile, your platform will benefit from the extra promotion, reputation support and greater revenue.

The important thing for all of these steps is to find a reliable development provider with fintech expertise who can guide you through the nuts and bolts of the technologies and features your product needs.

Fintech app features and tech stack

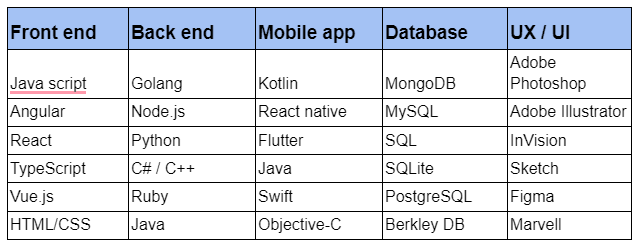

Choosing the technology stack is one of the crucial steps. Your choice sets the parameters for the end product. A suitable technology stack should enable you to build a fintech platform that's easy to maintain and upgrade. A good decision is best made by trusting specialists in this field.

Nevertheless, here are some suggestions. The most popular front-end technologies are JavaScript with Vue.js or React.js. Backend development can be done with Python, Java, Scala, and Golang. Mobile apps for fintech are typically written in Swift for iOS and Kotlin for Android. For those who would like a cross-platform app, React Native and Flutter are excellent options.

List of technologies possible to use for creating a fintech app. For more details on the development goes, check our post on the software development process and the principles MadAppGang believes in.

As for the set of features, it will largely depend on the type of app you want to build, but some are universal to the fintech industry:

- Login – It should be bullet-proof secure and future-proofed by incorporating several types of biometric authentication.

- Account details – Whether the app is connected to a financial institution or not, it has to allow users to sync their accounts and set permissions and limits. If you’re planning a banking app, in our other post you can find a detailed description of a banking app’s major features.

- Payments and transfers – This functionality lies at the core of most fintech solutions and should be easy to access and use. It also makes sense to design a convenient transaction history report, receipt sending options, and flexible recipient search. If you have an idea for a peer-to-peer payment app, our article on payment app features will come in handy.

- Analytical dashboards – When financial data is not just collected but also automatically analysed, it gives users valuable insights into their finances, be it personal budgeting or enterprise expense planning. Analytics are key to investment and trading apps as well, giving users tangible information about the current state of the market and possible risks and profits.

- Support and assistance – Most fintech apps feature either an option to contact support or a virtual assistant (chatbot or voice-enabled helper) that provides users with answers or directs them to the relevant information.

- Notifications – Any app should provide users with factual messages about their activity, as well as motivational incentives to perform certain actions.

The cost of fintech mobile app development

Mobile app development cost is defined by the set of features and the rates of the engineers working on a project. The more complex the product — the more features it has, the more unique they are, the more innovative the technologies involved — the more expensive the development will be.

In turn, the budget needed for each feature will depend on the cost of hiring app developers, designers, and testers. Their rates vary based on location, type of employment, and years of experience. For instance, you have the choice to go with generally cheaper individual freelancers or outsource to a dedicated team that is more expensive, but also more organised and committed as a whole.

Some sources claim simple fintech solutions might cost somewhere from $30,000 to 40,000, but from our experience, financial apps involve a lot of extra effort on security, regulatory compliance, performance stability, and integrations, which brings building a feature-rich application to an estimate of $500,000 and higher.

Cost-efficient alternatives

As an alternative to traditional development, there are opportunities to create a white-label app, which means customising a predefined set of designs and features. Several industry players offer fintech-specific white label apps, for example, Hydrogen Wealth allows building web or mobile robo-advisors and configuring your data in their templates. This option can pay off if you want to replicate functionality that has proven successful for other digital finance companies. But if you’re looking to design a unique and easily scalable app, you should choose traditional fintech mobile app development over white label.

Another beneficial alternative is low-code and no-code tools that can help you economise and significantly speed up the process. However, they also take a team of seasoned fintech app developers to apply everything correctly and according to your requirements.

The wrap-up

The fintech sector holds many opportunities to reach a wide audience of users who are searching for smarter ways to handle money. The demand for solutions is higher than ever, so if you have an app idea, don’t miss the chance to market it. To build a fintech app that’s successful with users, you need to identify the particular problem it will solve, and to make it robust, you need to find an expert development team with industry knowledge.

At MadAppGang, we’ve built large-scale fintech solutions that prioritise security and scalability, and we know what it takes to create a performant financial app. Let us help you build your product using our expertise in fintech software development. Reach out, and let's talk about your fintech idea, the required technologies, and the scope of the work.